Week ahead

The reinvigoration of US inflationary drivers is a lifesaver

The news about the financial crisis is increasing day by day and makes the risk aversion in the market more than past.

In the last week, the markets’ concern about banking crises has decreased and now traders are focusing on economic data again.

Following the release of US consumption and personal spending data, the market is pricing in an equal chance (50%) of a 0.25% hike and no change in interest rates by the Federal Reserve at its May meeting, roughly unchanged from before the data release.

In the coming week, one of the most important news of the market is the US jobs data, which good data can be a strong point for the US dollar because we are a little away from the possibility of ending the interest rate hikes.

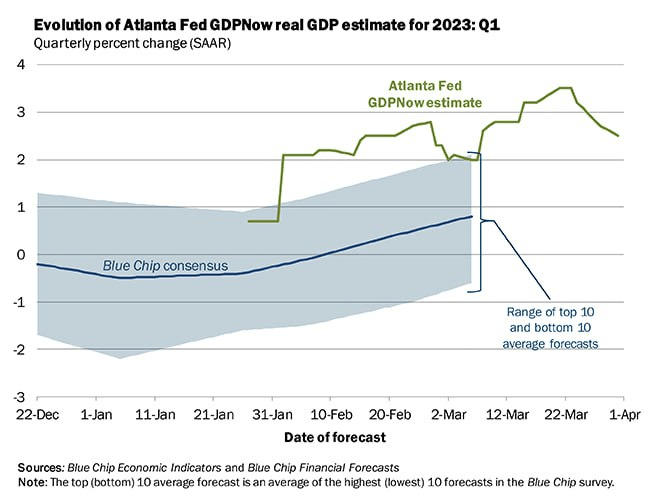

On the other hand, according to the GDPNow model’s latest estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2023, it was 2.5 percent on March 31, down from 3.2 percent on March 24. Currently, the growth of personal consumption expenditure, the growth of private gross domestic investment, and the growth of real government expenditure in the first quarter of this year have decreased from 5%, -7%, and 1.8% to 4.6%, -7.3% and 1.7% respectively, all of which They point to a revival of momentum in the US economy, improved demand, and a resurgence of inflationary drivers.

For the US dollar this week, the NFP (Ziwox calendar) employment report is expected to be 238,000, while the unemployment rate is expected to remain unchanged near 3.6%. These upbeat forecasts are supported by leading indicators such as the S&P Global business survey, which showed the fastest pace of employment growth in the previous six months.

If the rate of wage growth is surprisingly high, it could revive inflation concerns, delaying interest rate cut speculation until after the data helps improve the dollar’s strength.

Promising data for GBP

The UK government has announced its intention to join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), a free trade agreement between 11 countries including Japan, Canada, Australia, and New Zealand. This action is aimed at strengthening the UK’s business prospects after Brexit and strengthening relations with countries in the Asia and Pacific region. The agreement eliminates broad tariffs on goods and services and sets common standards on issues such as intellectual property and investment. This agreement covers a market of 500 million people and a total gross domestic product of 13.5 trillion dollars.

The UK economy grew in the last quarter of 2022 and avoided recession. England’s Office for National Statistics reported that gross domestic product, the value of all goods and services produced in England, increased by 0.6% in the fourth quarter of 2022, after falling by 0.1% in the previous quarter. This growth was caused by the increase in consumer spending and business investment, as well as the increase in exports.

This week we will have UK PMI data on Monday, Wednesday, and Thursday. Better-than-expected prints can increase the Sterling strength.

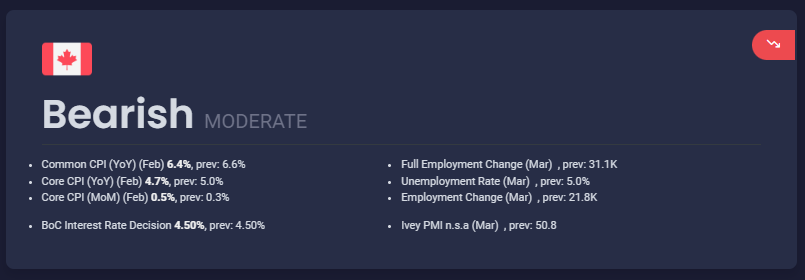

CAD Road map

Canada’s economy grew 0.5 percent in January, beating economists’ expectations and showing resilience despite rising Covid cases and supply chain disruptions. This growth was caused by the jump in retail and wholesale, manufacturing and mining, and oil and gas extraction. However, the services sector, which accounts for about two-thirds of Canada’s economy, declined slightly due to restrictions on dining and indoor recreational activities in some provinces.

Canada’s January gross domestic product also rose 0.5 percent from the previous month in last week’s report, while the market expected a 0.3 percent increase. Additionally, the preliminary estimate for February data was 0.3 percent, a sign of continued strong growth, despite a rapid decline in house prices and high-interest rates.

The Bank of Canada had forecast growth of 0.5 percent in its first-quarter forecasts released in January. The market is pricing in an 85% chance that the Bank of Canada will leave interest rates unchanged at its next meeting on April 12, with a 15% chance of a rate cut. Canada’s employment report is released on Thursday, a day ahead of the US employment report, and could be a roadmap for CAD and the next BOC interest rate decision.

Australia, End of the interest rate hikes?!

For the Australian central bank, BOA is expected to halt its contractionary cycle at Tuesday’s meeting. Traders have considered only 15% probability of an interest rate increase and 85% probability of no interest rate increase.

Expectations for an end to contractionary policies have been dampened by a disappointing set of data.

Retail sales figures and lower inflation have convinced investors that the Reserve Bank of Australia will not raise interest rates.

There are also many concerns about the housing market, as Australia has a high proportion of adjustable-rate mortgages that are re-rolled at higher interest rates, thus directly impacting homeowners.

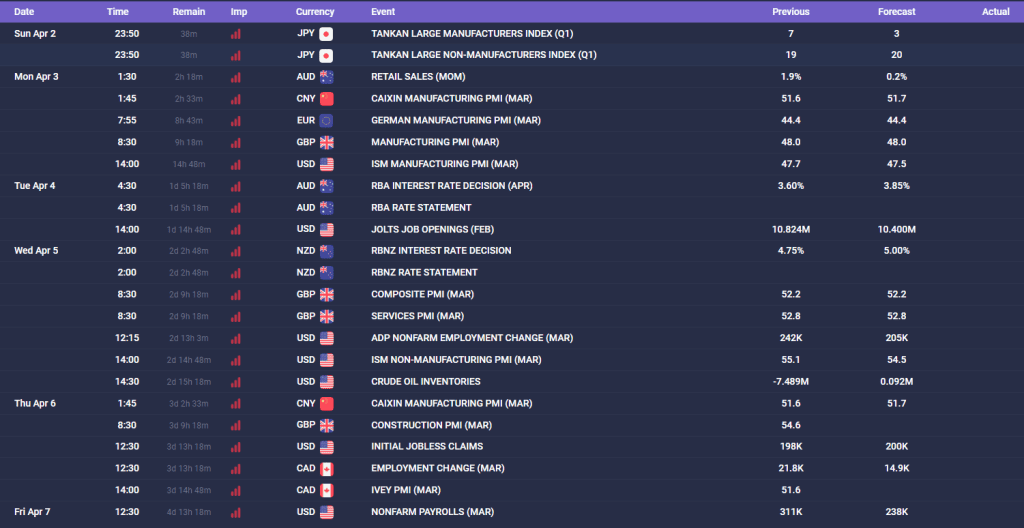

Economic calendar

Important event for this week:

Mon Apr 3:

- ISM MANUFACTURING PMI (MAR)

Tue Apr 4

- RBA INTEREST RATE DECISION (APR)

- JOLTS JOB OPENINGS (FEB)

Wed Apr 5

- RBNZ INTEREST RATE DECISION

- SERVICES PMI (MAR)

- ADP NONFARM EMPLOYMENT CHANGE (MAR)

- ISM NON-MANUFACTURING PMI (MAR)

Thu Apr 6:

- INITIAL JOBLESS CLAIMS

- EMPLOYMENT CHANGE (MAR)

- IVEY PMI (MAR)

Fri Apr 7

- NONFARM PAYROLLS (MAR)

- UNEMPLOYMENT RATE (MAR)