Week ahead

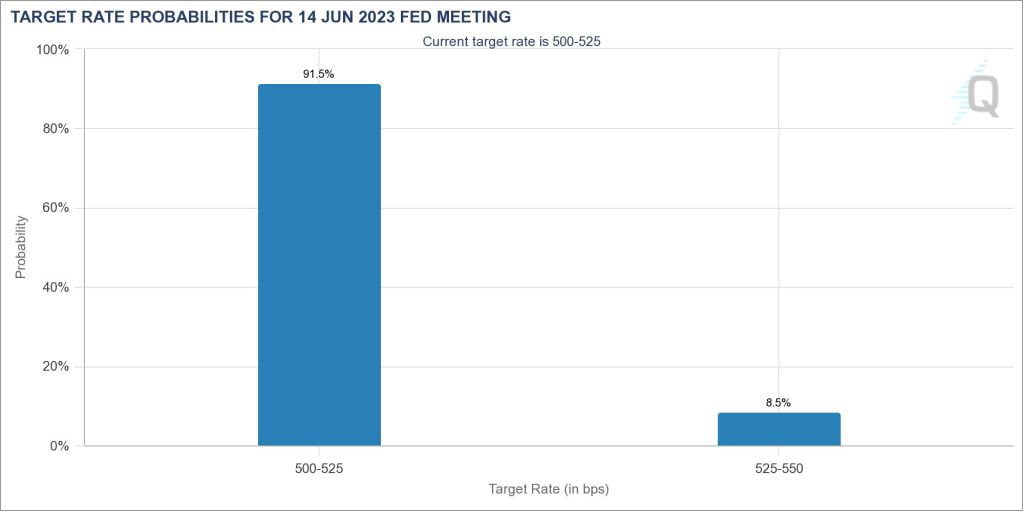

End of interest rate hikes by FED

🇺🇸 For the US dollar, the CPI index for April, due out on Wednesday, will be on everyone’s radar. The core CPI data is expected to change from 5.0% to 5.2% year-on-year, while the core CPI rate is expected to be unchanged at 5.6% year-on-year, indicating that the increase in the cost of factory goods accelerated during the month.

Also, the U.S. Nonfarm Payrolls data and last week’s US jobless claims released rose by the most in six weeks, a sign that the US labor market may be weakening. For this reason, this week’s inflation can be very important because the reduction of inflation along with the pressured job market can provide peace of mind for the Federal Reserve.

Note that investors also expect interest rates to fall by more than 0.75% by the end of the year.

Specifying the policies of banks turn by turn, Now for BOE

🇬🇧 After a turbulent week for the European Central Bank and the Federal Reserve, it is the Bank of England’s turn.

In its last meeting in March, the Bank of England increased the interest rate by 0.25% this time after increasing it 10 times.

BOE officials downplayed the surprise rise in inflation in February and focused on their next steps, saying more accommodative policy would be needed if there was evidence of sustained price pressures. The view that European banks, including the UK, are better supervised than US banks appears to have been partly supportive of European currencies. This raises the expectation of traders and analysts to predict interest rate hikes several more times for the BOE.

Since then, data has shown that inflation has eased less than expected and the core inflation rate has remained marginally above 10 percent year-on-year, allowing investors to see around 0.6 percent more rate hikes by the end of this year. price For next week’s session, investors are roughly 85% likely to see interest rates rise by 0.25%, with the remaining 15% likely to hold interest rates unchanged.

Therefore, the market has well-priced the pound’s currency strength with a 0.25% hike, so what causes more rapid growth is a surprise greater than 0.25%.

What could further dampen the bullish outlook for the pound could be a bigger-than-expected decline in Britain’s first estimate of first-quarter gross domestic product (GDP), which is due to be released on Friday alongside the country’s trade data for March.

China, Australia, and New Zealand

🇦🇺 🇳🇿 🇨🇳

Trade data from the world’s second-largest economy and Australia and New Zealand’s main trading partner (China) is due on Tuesday and may be of interest to traders for the New Zealand dollar and the Australian dollar.

After China’s PMI data disappointed traders last week, the release of weak trade data this week could indicate that China has yet to return to its previous decline after declaring the end of the Coronavirus in the world.

China’s Consumer Price Index (CPI) and Producer Price Index (PPI) will be released on Thursday.

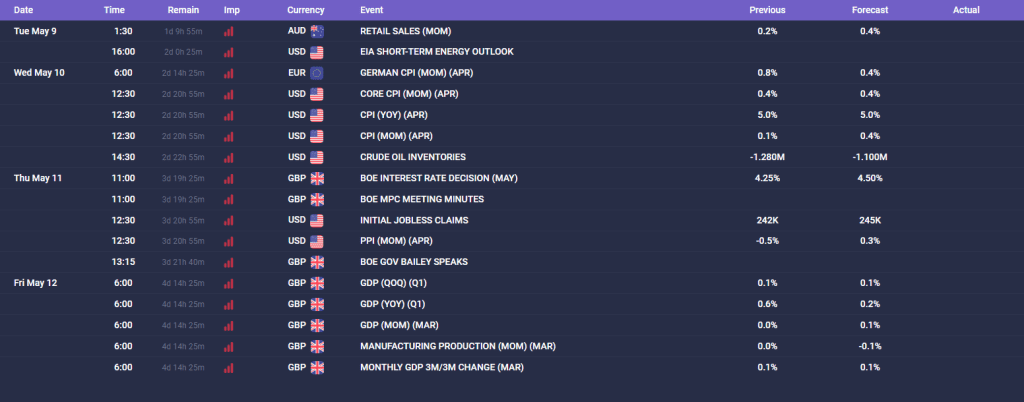

Economic calendar

Important news/events for this week are:

Thu May 9:

🇦🇺 AUD RETAIL SALES (MOM)

Wed May 10:

🇩🇪 GERMAN CPI (MOM) (APR)

🇺🇸 USD CPI & CORE CPI (MOM) (APR)

Thu May 11:

🇬🇧 BOE INTEREST RATE DECISION (MAY)

🇺🇸 USD INITIAL JOBLESS CLAIMS

🇺🇸 USD PPI (MOM) (APR)

Fri May 12:

🇬🇧 GDP index

Leave a Reply

You must be logged in to post a comment.