Weekly Forex Analysis

Week ahead

Dollar, goes up and down with other currencies

🇺🇸 The recent economic data for the United States has been disappointing, leading investors to reconsider the necessity of another interest rate increase by the Federal Reserve before the contractionary phase concludes, potentially followed by more rate cuts next year. Consequently, the US dollar has shown signs of weakness in the financial markets.

This week, the dollar’s calendar is relatively uneventful. If economic data from other countries is released with weak figures, it could bolster the dollar’s strength. Conversely, if this data appears weak, it may lead to a correction in the dollar’s value. In the event that both the dollar and other currencies weaken, there is likely to be increased demand for the dollar as it is perceived as a safe asset.

It’s a funny theory Dollar Smile Theory

When the future outlook is abnormal, the demand for the dollar will be checked. If it rises, the dollar will be corrected and vice versa from this week. In the past, the sentiment of the market is risk-averse and it will continue on Monday, the dollar may not correct before it changes.

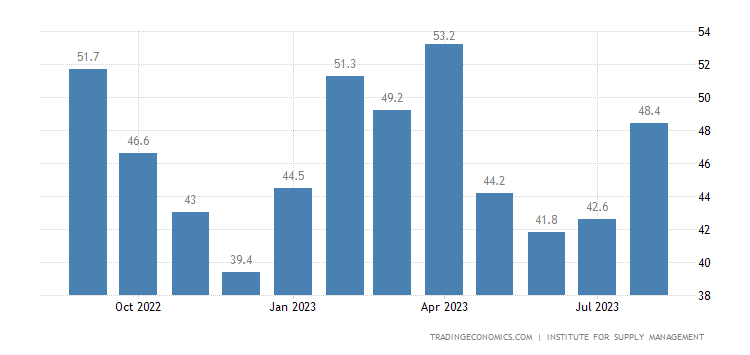

After a barrage of disappointing data for the US dollar in the past week, investors are now wondering whether another rate hike by the Federal Reserve is needed.

This week, more attention will be focused on the purchasing managers’ index of the US service sector, as reported by the ISM Institute. Both the preliminary Purchasing Managers’ Index of the manufacturing sector and the services sector from the S&P Global Institute increased the market’s expectations for no increase in interest rates and even a decrease in August. Taking this issue into consideration, the possibility of a decrease in the ISM index in the next week has also increased. However, reducing the likelihood of another rate hike by the Federal Reserve will also depend on the sub-indices of new orders and prices. If we see declines in these two categories as well, the US dollar and Treasury bond yields may remain under pressure and the stock market will continue to rise, as rising expectations of interest rate cuts could reduce the net present value (NPV) of companies with good growth.

Mixed EUR

🇪🇺 Quietly, the “stagflation” scenario is making a comeback in discussions about the Eurozone’s economic future. The European Central Bank (ECB) has acknowledged that economic growth will be much weaker than their initial forecasts, and core inflation remains stubbornly above 5%. The ECB is expected to maintain its planned 0.25% rate hike at the September meeting, but some believe this could be a mistake.

Meanwhile, eurozone leaders are still considering whether to reinstate the Maastricht debt and deficit measures that were temporarily suspended during the pandemic. While this move might benefit government bond markets in the eurozone, it could have a negative impact on the euro due to less expansionary monetary policies and more contractionary fiscal policies. Prior to the pandemic, there were discussions about keeping the budget deficit below 3% of GDP.

This week, no important data will be released for the Eurozone.

Bank of England Decision Survey

🇬🇧 The Office for National Statistics (ONS), which is Britain’s national data office, provided assistance to UK policymakers on Friday. They revised the GDP growth for 2021 to 1.7%. This indicates that the UK has achieved pre-pandemic growth earlier than previously estimated. As a result, Germany now appears to be the weakest performer among G7 countries in the post-pandemic period. This revision may also give the government more financial flexibility, and it wouldn’t be unexpected if there’s increased speculation about potential financial measures in the Chancellor’s Autumn Statement in November.

British stock market is at high levels, the sentiment is weak and if the British PMI is published in the weak service sector, it will put more pressure on it. Technically, we are close to a mid-term support level, and like the Euro, we can have a recovery movement to the price volume area in the event of a break, and with the failure of the floor and pullback, the downward trend will continue to lower levels, which will be updated, in general, if possible. The price of maintaining this floor is placed in a range box.

High-risk market assets

The Australian dollar, Canadian dollar

🇨🇦 BOC will hold a meeting on Wednesday and decide on the interest rate. Their previous decision was to raise interest rates by 0.25 percent, and on the other hand, low inflation data for Canada reinforces this assumption for not raising interest rates. Inflation in Canada is currently higher than the Bank of Canada’s 2% target. However, since Canada’s core inflation rate is closer to that target compared to other major economies, Now adopt a wait-and-see approach to determine whether the past interest rate hikes continue to put downward pressure on prices or not. Anyway, Possible gains for the Canadian dollar after the central bank meeting may depend largely on Friday’s employment report for August.

🇦🇺 Interest rate decision on Tuesday, Sep 5. Its result can influence the market’s expectations about the future path of monetary policies of other currencies. Australia’s central bank officials did nothing to interest rates in the previous session. Expectations again for the bank to keep interest rates unchanged, the unemployment rate in Australia has increased from 3.5% to 3.7%, and core inflation in Australia has decreased from 5.4% to 4.9% annually, which makes the possibility of no interest rate hike for Australia.

Economic calendar

Important news/events for this week:

Leave a Reply

You must be logged in to post a comment.