Dollar rise again

The recent financial markets have been driven by sentiments, particularly revolving around the United States debt ceiling issue. Treasury Secretary Janet Yellen has raised concerns about a potential default in June if Congress fails to extend it. President Joe Biden and senior Congress members are actively negotiating to resolve the matter, which mainly centers around spending levels. Opposition Republicans have indicated a willingness to raise the debt ceiling if the Government accepts spending cuts.

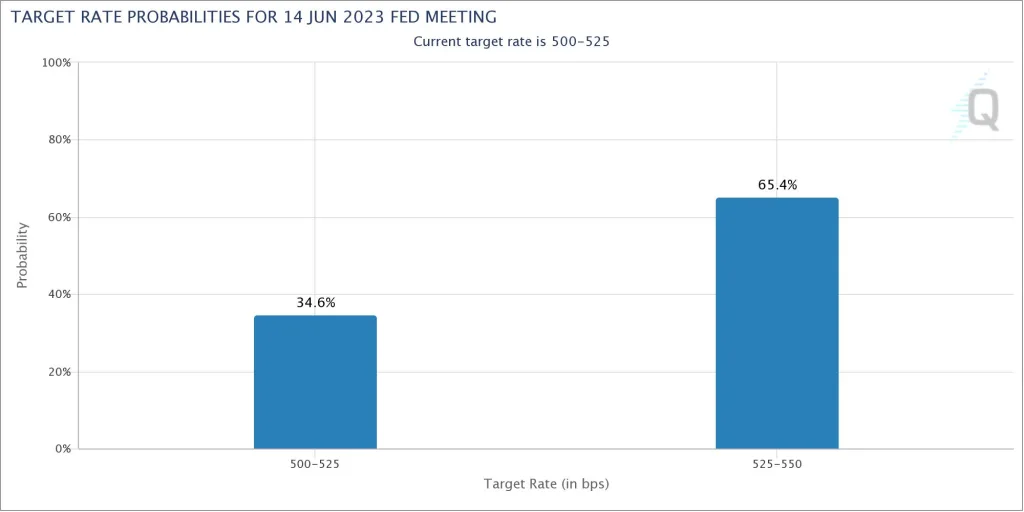

Market expectations of a Fed rate hike rose to 65% after positive macroeconomic data and higher inflation figures were reported. According to the CME FedWatch Tool, the Fed is projected to hike at the 13th meeting, with interest rates predicted to rise by 0.25 percent on June 14.

Overall sentiment has turned more hawkish on the Fed, and if the debt ceiling crisis is resolved favorably and next Friday’s NFP prints more than expected, a rate hike in June seems more likely.

The next round of US employment data (NFP) on Friday is very important.

Forecasts for the US non-farm payrolls report added 180,000 jobs in May, which was less than the previous month, but still a significant figure. The unemployment rate is expected to rise to 3.5 percent, but wage growth will pick up slightly over the year.

This week, Investors will be watching the payrolls and UNEMPLOYMENT RATE. the result is Fed’s next moves, as any unexpected changes in policy could lead to significant market volatility. In the meantime, traders are positioning themselves for a potential rate hike, with many betting on a stronger dollar and higher bond yields in the coming months.

Interest rate expectations rice due to the UK inflation

UK inflation rate has hit single digits anew, though it has not attained the number foreseen by economists. The United Kingdom’s net inflation growth has surged to the same level as ten years ago.

Expectations are high for a Bank of England interest rate hike soon; from 4.5% to a minimum of 5%, and possibly even as high as 5.5% to curb inflation’s swift expansion, according to financial market predictions.

Inflation figures have impacted the British bond market leading to heightened interest rate expectations, resulting in government bond yields rising to a multi-month high and investors anticipating increased bond yields.

We don’t have any important calendar for GBP this week, but the US economic calendar is busy with the full US employment report or NFP on Friday. Continued strong growth in the US labor market will increase the interest rate of the Federal Reserve, favoring the US dollar and harming the GBPUSD currency pair. The US government and parliament are close to a debt agreement, with a deadline of June 1st, and delays will harm the US economy.

Eurozone and failure to grow

Euro had an uneventful week. Euro remained feeble versus USD and struggled against GBP. It has slumped against USD uninterruptedly for four weeks.

ECB officials continue to favor interest rate increases, yet this stance hasn’t visibly impacted the euro. This may be due to the fact that the ECB’s rate hikes have translated into higher prices, rendering the official’s hawkish outlook ineffective in shaping interest rate forecasts.

Next week, Eurozone will release inflation data, but the forecast suggests that significant deviation from expectations in the inflation data of the euro area is unlikely.

The main driver of the EURUSD currency pair is again the US dollar and the news related to the negotiations on the debt ceiling of the US federal government. In the meantime, the US NFP employment report will be very important for the market.

Release of data from China, Canada, and Australia

On Wednesday, the newest purchasing managers’ index (PMI) figures will be disclosed in China. As China’s economy has recently lost strength with the fading of the reopening boom, the results of these surveys will display if the disquieting trend persisted in May. In case it did, the currencies of countries such as Australia and New Zealand, which rely on Chinese demand for their exports, may undergo additional decline.

The fundamental bias of AUD and NZD is Bearish and the forecast is Bearish too.

The release of the latest purchasing managers’ index (PMI) figures in China on Wednesday will be closely watched by investors and analysts alike. With the country’s economy experiencing a slowdown in recent months, the PMI results will reveal whether the trend continued into May. If so, this could have detrimental effects on the currencies of countries heavily reliant on Chinese demand for their exports, such as Australia and New Zealand. As such, many will be keeping a keen eye on the figures to gauge the health of China’s economy and the potential knock-on effects on the global market.

Economic calendar

Important news/events for this week:

Latest post

- GBPUSD Trade idea: Bearish Pressure Builds Ahead of UK Political Risk and Strong USD Momentum

- What to Buy in the Russia–Ukraine War? Best Assets to Profit from the 2026 Geopolitical Crisis

- Germany’s Industrial Rebound Strengthens, but Trade Risks Cast a Shadow

- Forex Weekly Outlook, Cooling US Inflation, Monetary and Year-End Risks

- Forex Weekly Outlook: Navigating Risk, Data, and Central Bank Divergence

Leave a Reply

You must be logged in to post a comment.