Quite simply, the balance sheet of the Federal Reserve or the balance sheet of the Central Bank of America is a financial statement that shows the assets and liabilities of the Federal Reserve. This balance sheet is published weekly and is called the H.4.1 statement of the Federal Reserve.

Increasing the balance sheet means increasing liquidity. The work that Federal Reserve had started hawkish monetary policies to control it.

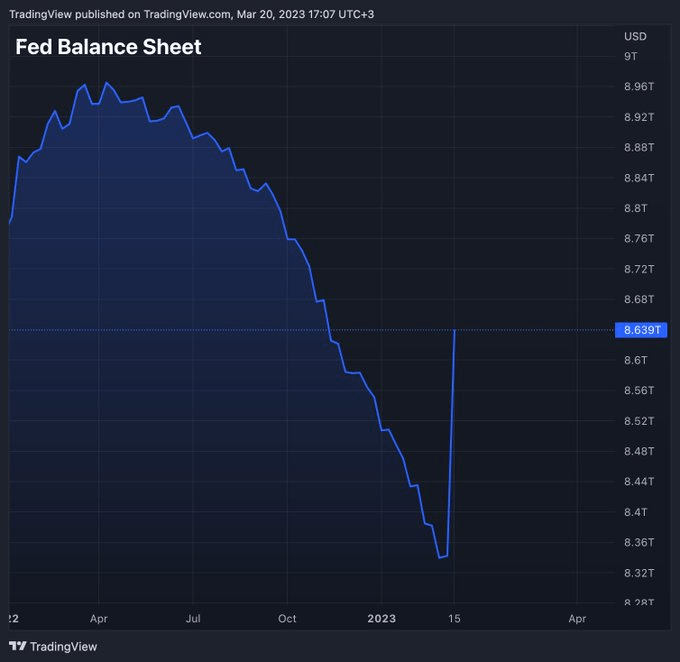

NOW! The US Federal Reserve’s balance sheet increased by $297 billion this week to $8.63 trillion, the highest level since November. This increase follows the new policy of the Federal Reserve to save banks in a crisis of liquidity, such as Silicon Valley and Signature. Following the increase in the balance sheet of the Federal Reserve, the price of Bitcoin and Ethereum has increased in the last 24 hours.

A year of trying to raise interest rates and reduce the balance sheet resulted in a few days. The balance sheet of the Federal Reserve, which had been reduced with great effort, increased in a spike last week due to economic pressure and the addition of financial and banking crises.

Now the question that arises is whether the Federal Reserve will continue to raise interest rates?

According to reports, US banks have borrowed a total of $164.8 billion from the Federal Reserve. Due to the fear of bankruptcy, amount of loans taken from the Federal Reserve by banks increased from 4.58 billion dollars in the past week to 152 billion dollars on March 15. Previously, the highest amount of loans taken from the Federal Reserve took place during the 2009 financial crisis, during which banks received a total of $111 billion in financial aid from the US government.

Now, with this incident, the balance sheet of the Federal Reserve has greatly increased, and its effect on the markets will be the growth of gold and the growth of cryptocurrency.