Dollar remains overvalued

Raffi Boyadjian

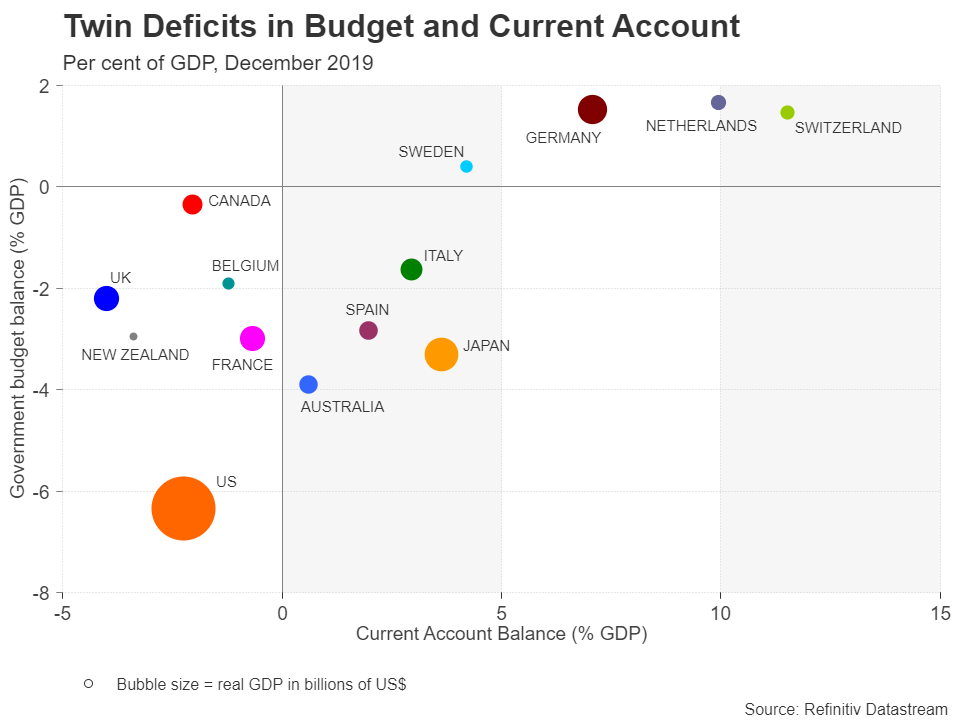

Can America’s twin deficits still sink it?

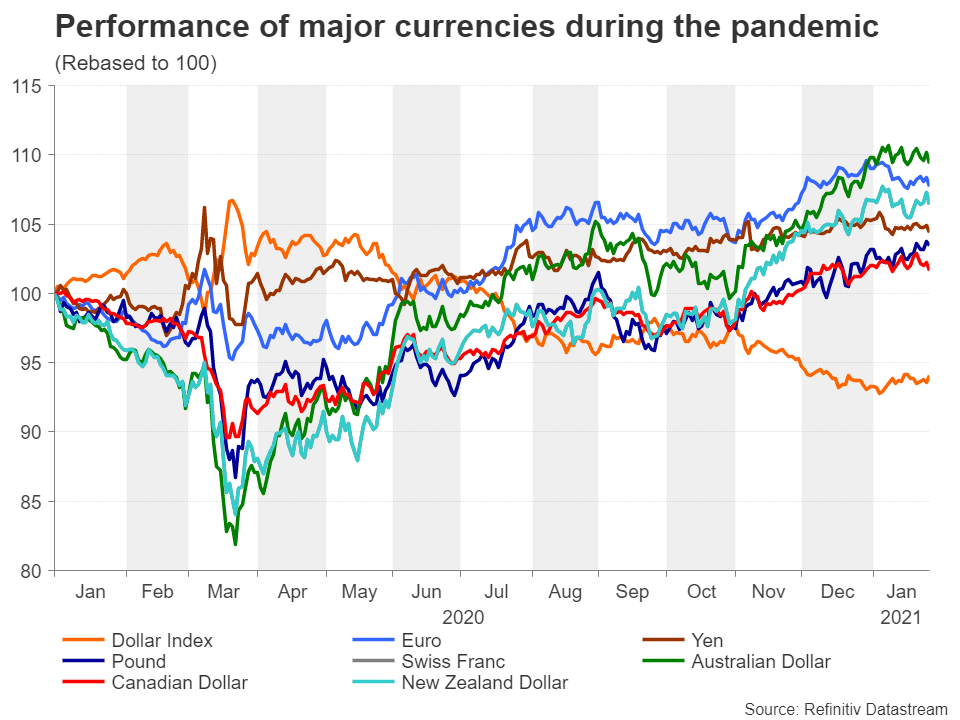

The US dollar ended a volatile 2020 down 6.5% against a basket of currencies, underlining the dramatic turnaround in risk appetite from the depths of the March virus crisis. That risk rally is showing no sign of abating anytime soon, driving bearish bets against the dollar to near-decade highs. Nevertheless, the dollar’s negative outlook is becoming increasingly murky as the US economy is poised to outperform its peers in 2021. In view of this, can America’s soaring current account and budget deficits keep the dollar firmly skewed to the downside? Comparing the US’ twin deficits and the exchange rate as implied by purchasing power parity (PPP) to those of other advanced economies, the odds are stacked in favor of the bears.

Dollar still top of the pack

Policymakers have long held issues with market-set exchange rates as they are often distorted by a host of factors, though speculative trading is often seen as the biggest ‘evil’ force that tends to undermine the concept of free-floating currencies. One of the more popular metrics economists look at to decide whether a country’s currency is overvalued or undervalued is the famous Big Mac index devised by The Economist. It measures PPP by comparing the price of a Big Mac (which is prepared using the same locally sourced ingredients) in each country and converted to dollars.

In January’s bi-annual update of the index, there were only three currencies more overvalued than the dollar, suggesting 2020’s downtrend didn’t go far enough. One of those currencies, as you would expect, is the Swiss franc, which is 28.8% overvalued against the greenback. The Canadian dollar (-6.6%) is the least undervalued among the major currencies, followed by the euro (-8.8%), Australian dollar (-11.9%), New Zealand dollar (-13.9%) and pound (-21.6%). Surprisingly, the most undervalued is the Japanese yen.

Yen: a cause for a US-Japan row?

At 33.9% undervalued, the Japanese currency, which regularly features in the US Treasury Department’s currency manipulation reports, is at risk of coming under sharper attack from Washington in 2021. The dollar has been trading within close vicinity of the 100-yen level since late last year. Should Japanese authorities be tempted to intervene to keep the pair above the 100 threshold, the Treasury Department is unlikely to let it go unnoticed.

Another argument in dispu

te of a weaker yen is Japan’s healthy current account surplus. The better a country’s current account position, the stronger the case for a currency to appreciate, as surplus countries are not dependent on foreign capital inflows to finance a deficit. In contrast, the United States has been running a huge current account shortfall for decades and former President Trump’s protectionist policies did little to reduce the trade gap.

The unwanted title of a safe haven

At the opposite end of the table, Switzerland has an even larger current account surplus, making it a net creditor nation like Japan. This enviable position has earned the yen and franc the status of a safe haven. But why is there such a discrepancy between the PPP exchange rate for the two currencies?

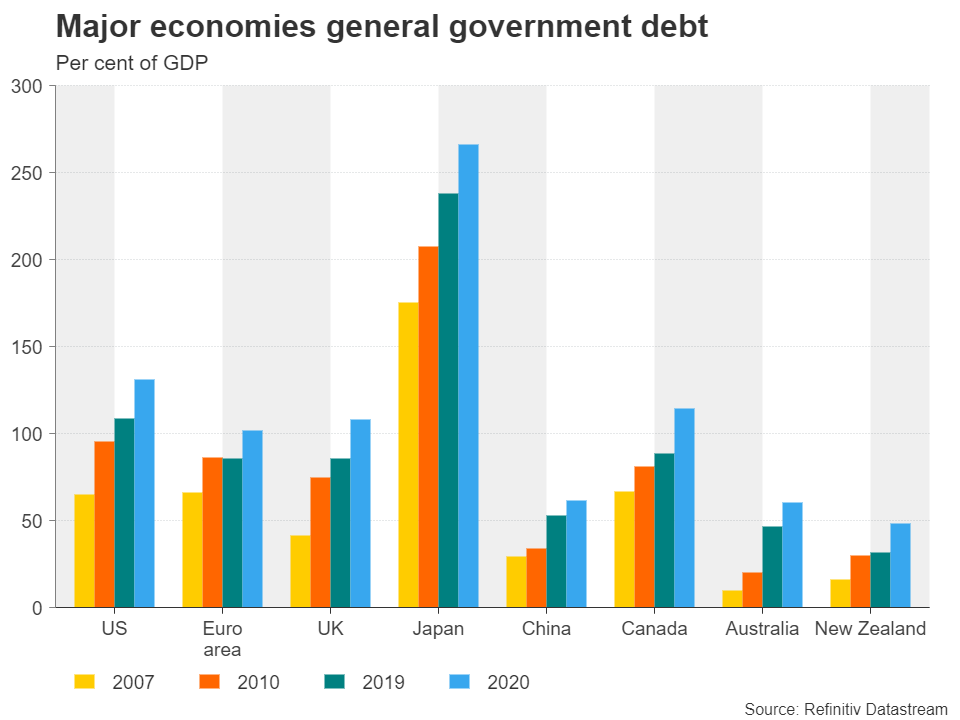

Differing approaches to monetary policy is one explanation as to why the franc remains greatly overvalued and the yen too weak on a PPP basis. The Bank of Japan’s years of quantitative easing (QE) has made it the biggest holder of Japanese government bonds by a wide margin. QE tends to depress a country’s sovereign bond yields, weighing on the currency. But for a central bank to be able to buy vast quantities of government bonds, there has to be enough supply, and there has been plenty of that in Japan. The Japanese government has been running massive budget deficits since the 1990s and this is what distinguishes Japan with Switzerland where government borrowing is better managed.

Euro’s troubles are never over

Several other European nations also have a sizeable current account surplus, the most notable one being Germany. The euro area as a whole happens to be in a surplus with the rest of the world too. But the Eurozone’s endless economic and political woes have been a thorn in the euro’s side. The economy’s poor performance since the 2008-09 financial crisis has converted a once hawkish European Central Bank into one of the world’s most dovish central banks.

Nonetheless, the pandemic did not stop the euro from enjoying a good year against the dollar in 2020. The pair rallied almost 9% last year, but the ECB is already getting itchy and is exploring ways of stemming the single currency’s ascent. Unlike the Swiss National Bank and Bank of Japan, forex intervention is not a realistic option for the ECB so policymakers have to be more creative at how they can maintain a competitive exchange rate. However, judging by Eurozone governments’ sketchy response to the pandemic, both in terms of speeding up the recovery and the vaccination programme, the euro may have already peaked. Thus, expectations that euro/dollar will extend its uptrend in 2021 may be too optimistic.

Pound injected with vaccine hype

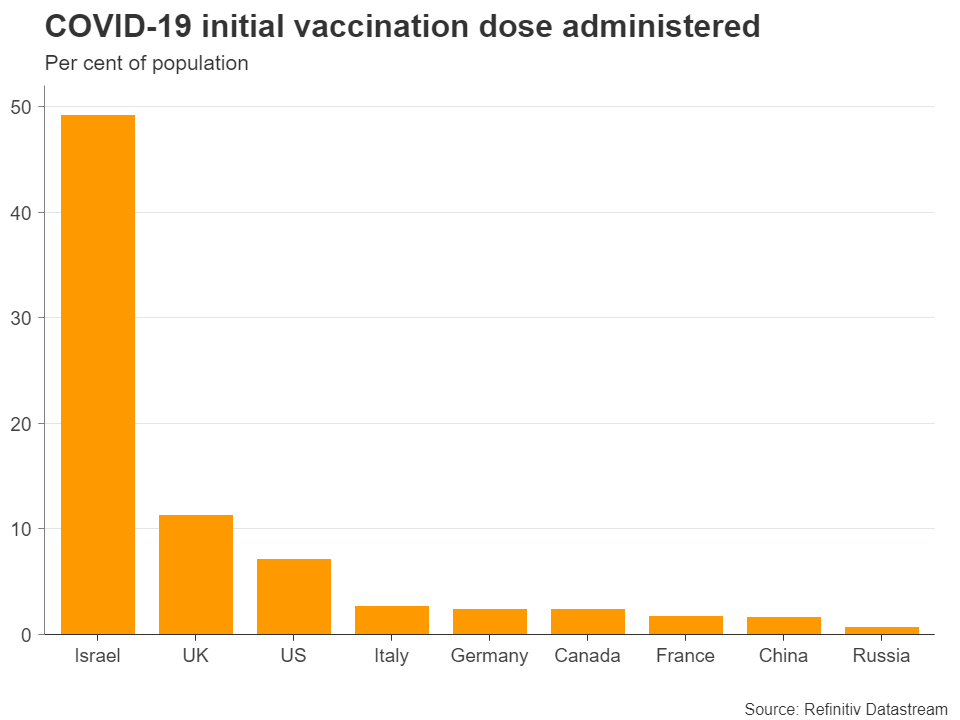

Across the channel, the UK economy isn’t faring any better. Yet things are looking up for the pound, which climbed to fresh highs against both the dollar and euro in January. Britain’s relative success in rolling out vaccines across the country at an impressive rate has given investors hope that lockdown number three will be the last and the economy can fully reopen by the end of the year. Sterling is the next cheapest currency after the yen according to the Big Mac index so a further appreciation might not be irrational at all.

However, the United Kingdom has a twin deficit problem of its own, making the pound highly susceptible to global crises and risk-off moves. Furthermore, the pound is only attractive against the current backdrop because its peers are doing worse. In a future where vaccinations have covered 80% or more of the world’s population, Brexit could once again take centre stage for sterling as the existing trade deal with the EU is already showing cracks and may not be sustainable as a long-term solution.

Aussie, kiwi and loonie fare not too badly

As for the commodity-linked dollars, they are similar to the pound in that Australia, Canada and New Zealand run a current account deficit in most years. Hence, their currencies are largely driven by risk sentiment, which is quite closely correlated to growth in world trade. But while the Australian, Canadian and New Zealand dollars are hugely exposed to changes in demand for commodities, they are not as vulnerable as the pound, which relies more on volatile capital inflows into the City of London. This, together with Britain’s deteriorating national finances, might partly explain why they are less undervalued than the pound.

Have markets become too optimistic?

So where does all this leave the US dollar? The continued PPP-implied strength of the mighty greenback even amidst the weight of worsening twin deficits and a pledge by the Federal Reserve to stick to ultra-loose monetary policy for the foreseeable future is quite startling. But maybe not. There may be a lot of optimism in the markets right now, but the global economy is nowhere near out of the woods just yet as far as the pandemic is concerned. That optimism is one half fed by the abundance of liquidity and expectations of even more stimulus and one half by hopes that immunization against Covid-19 will bring an end to social-distancing rules.

US economy still has the edge

However, the US is not only likely to receive the largest fiscal stimulus from all the virus-hit countries, it’s also one of the few that’s vaccinating its population at an adequate rate. The Eurozone, in comparison, is trailing behind on both fronts, the UK’s Brexit problems may only be just beginning, Japan is juggling deflation again, and the export-dependent economies of Australia, Canada and New Zealand might hit a stumbling block if the recovery elsewhere falters, particularly in China, which has had to tighten virus restrictions lately.

The dollar’s downslide is already showing signs of bottoming out and a period of consolidation seems more than reasonable given the many risks that still lie ahead. Meanwhile, rising inflation expectations in the US are another challenge for the dollar bears. Until some of the fog is lifted and the economic outlook for America’s rivals brightens up a bit more, it will be difficult for those currencies to stretch their 2020 gains much further in 2021.

Dollar’s day of reckoning probably not near

That’s not to say, though, that the twin deficits won’t pose a problem for the dollar. After all, with President Biden’s spending plans expected to take the US debt-to-GDP ratio to new heights and the extra stimulus widening the current account deficit even further as imports are boosted, there’s bound to be a day of reckoning. However, that day is more likely to come in 2022 or possibly even later, when the global recovery is on a steadier footing and vaccinations are well underway in most countries.

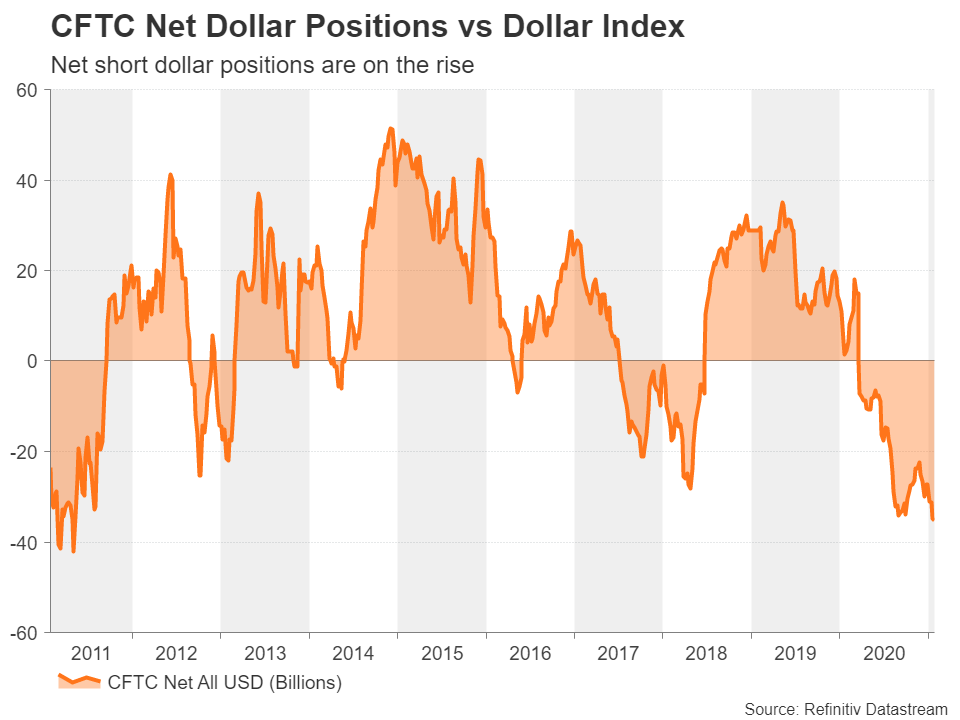

Aside from these imbalances, the case for a weaker dollar is further supported by the implied value of the Big Mac index as well as the continued rise in dollar net short positions (according to CFTC data). But until there’s a more convincing economic rebound elsewhere, it will be a while before the pandemic-era safe haven trades, which are propping up the greenback, are fully unwound.