The Bank of New Zealand’s impending decision to hold interest rates at 5.5%

New Zealand’s central bank’s ongoing efforts to maintain restrictive measures highlight the intricate balance required between actively managing inflation and safeguarding a moderately evolving economy. The Bank of New Zealand’s decision to pause its series of robust rate hikes in July, following an aggressive spree last year, acknowledges the evolving economic landscape where price pressures are gradually subsiding. However, the intricate interplay between waning economic momentum and the persistent concern of delayed rekindling of inflation presents a multifaceted challenge to price dynamics. Experts and financial analysts, finely attuned to the nuanced dynamics of these elements, find themselves at the juncture of two divergent potential paths. The prevailing market consensus suggests that the New Zealand central bank’s tightening phase has concluded, potentially paving the way for an impending interest rate reduction in the first half of the coming year. Nonetheless, substantial dissent exists, with financial institutions ANZ and Westpac endorsing an additional 0.25% rate hike by the end of 2023 from the New Zealand central bank.

The impending conclusion approaches for the eagerly awaited release of the Reserve Bank of New Zealand’s report, a key component of the upcoming quarterly monetary policy statement. The comprehensive report, featuring revised interest rate projections spanning three years, offers insights into the strategic path chosen by the Bank of New Zealand. Despite economic growth’s significant role in shaping the inflation perspective, experts concur that economic activity is on track for further moderation in the latter part of 2023 and the subsequent year. The intricate ramifications of the interest rate adjustments present a multi-faceted scenario, impacting aspects ranging from household finances to broader sectors like manufacturing and real estate. The gradual shift toward higher interest rates, though not yet profoundly impacting homeowners with fixed-rate mortgages, is projected to curtail consumer spending. This trend mirrors the narrative in the manufacturing sector, which has weathered the strain of five consecutive months of contraction, mirroring the depths of the global financial crisis.

The vital real estate sector, fundamental to economic well-being, contends with a substantial 10% decline in housing prices over the last year, accompanied by a halt in sales volume—an occurrence mirrored within the construction industry. Amid New Zealand’s pursuit of its own domestic economic vitality, the reverberation of the global economic pattern is unavoidable. China’s evident deceleration in commodity demand has seeped into New Zealand’s economic projection, exemplified by dairy giant Fonterra’s projection of a 15% reduction in payments to local farmers for milk—a tangible manifestation of global consolidation. Amidst this backdrop, the influx of immigrants and the burgeoning growth in inbound tourism serve as shields against the prevailing obscurity. Concurrently, the influx of foreign labor gradually alleviates inflationary pressures on wages.

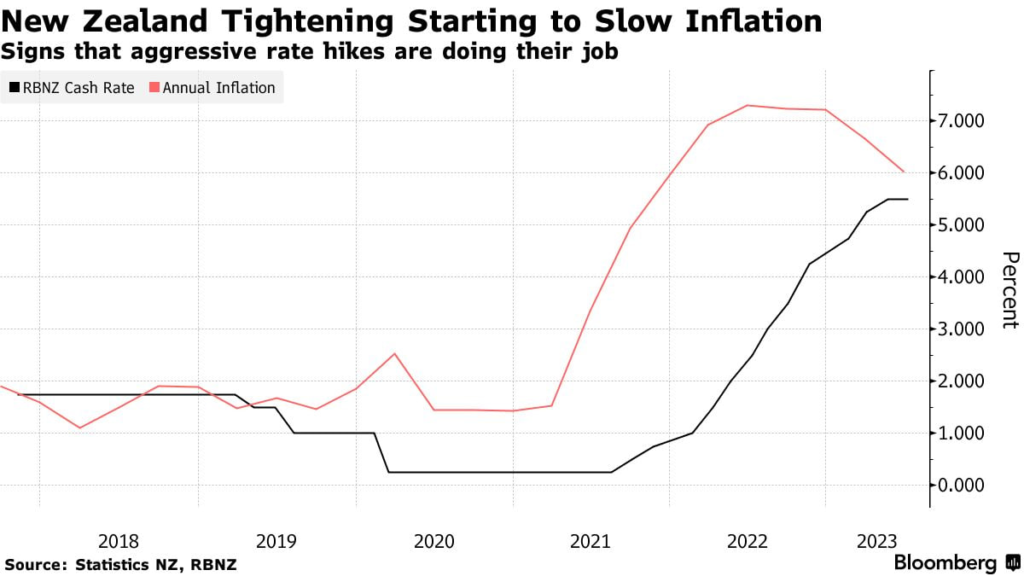

While the total inflation decreasing to 6% in the second quarter shows a more moderate path, the indicators of high domestic price pressure continue; With 2-year inflation expectations coming in at 2.83%, they are getting closer to the upper end of the New Zealand central bank’s target range. In parallel, the relentless rise in food prices, which saw a 9.6 percent year-on-year increase through July, continues to signal underlying resilience in price dynamics. As New Zealand’s central bank navigates these complex currents, Sharon Zollner, ANZ’s chief economist in Auckland, reminds us that caution remains a key focus for economists. The gradual erosion of inflation expectations may provide some respite for the New Zealand central bank, but persistent differences in target levels require vigilance. Zollner’s expectation of a final interest rate hike by the New Zealand central bank in November underscores the ongoing challenges in containing inflation and stabilizing economic growth.

Update:

Bank of New Zealand Monetary Statement: Interest rates should remain at restrictive levels for the foreseeable future

As expected and necessary, the current level of interest rates is restraining spending, and thus inflationary pressures.

The supply and demand imbalance is getting better.

As expected, New Zealand’s economy is expanding broadly.

The overall inflation rate and inflation expectations have decreased, but the core rate of this index remains high.

Our forecasts indicate the possibility of an interest rate increase in the fourth quarter of 2023.

Bank of New Zealand members are convinced that as long as interest rates remain at restrictive levels, the CPI will return to its target range of 1-3% per year.

We still expect inflation to fall below 3% in the third quarter of 2024.

Bank of New Zealand members noted that the index-based estimate of the nominal neutral interest rate had risen by 0.25 percentage points to 2.25 percent.

Bank of New Zealand members forecast that inflation will remain within the target range until the second half of 2024.

Leave a Reply

You must be logged in to post a comment.