SNB hikes rates by 25bp and signals further tightening still to come

25bp rate hike as expected

As expected, the Swiss National Bank has raised its key interest rate by a further 25 basis points to 1.75%. This brings the total amount of rate hikes in this cycle to 250 basis points in one year, well below the European Central Bank’s 400bp and the Federal Reserve’s 500bp. At the same time, the SNB continues to intervene in the foreign exchange market by selling currencies, thereby strengthening the Swiss franc and bringing down imported inflation. After years of foreign currency purchases, this reduces the size of the SNB’s balance sheet and is therefore a particularly effective form of quantitative tightening against inflation.

Long-term inflation concerns

This rate hike comes against a backdrop in which inflation remains above the SNB’s inflation target of between 0 and 2% – although it has fallen sharply. It reached 2.2% in May, a steady decline from the 3.4% reached in February 2023. Core inflation fell below 2% to 1.9% in May. Thanks to lower energy prices and the appreciation of the Swiss franc, the SNB expects inflation to continue to fall to 1.7% in the third quarter.

Despite this encouraging decline, the SNB continues to see inflation as a problem and expects it to strengthen over the coming winter due to second-round effects. Inflation is also expected to become increasingly domestic, and therefore less easily combatted by strengthening the exchange rate. Of particular concern is an expected rise in rents, which account for 16% of the consumer basket and are indexed to interest rates in Switzerland.

In light of this situation, the SNB has revised up its inflation forecasts for the next few years and now expects inflation to remain above 2% until the end of the forecast horizon in the first quarter of 2026. It’s expected to average 2.2% in 2023, 2.2% in 2024 and 2.1% in 2025. In other words, aside from the fall expected this autumn, the SNB does not expect any moderation in inflationary pressures and believes that the current situation is likely to persist. This signal growing concerns about the long-term outlook for inflation.

Another hike expected in September

This upward revision of forecasts is a particularly hawkish signal and suggests that the SNB will raise rates again. President Thomas Jordan almost pre-announced this at the press conference, stating that tighter monetary policy will be necessary to bring down inflation. As a result, we are now expecting another rate hike of 25 basis points in September.

At a time when other central banks seem to have lost confidence in their models and are looking primarily at the actual rate of inflation, the SNB seems to be taking a different approach by focusing primarily on inflation forecasts. The fact that the ECB is likely to be more aggressive than previously expected – probably raising rates again in July and September – should further reinforce the SNB’s decision. After September, the SNB rate is likely to remain at 2%, with a rate cut looking unlikely between now and 2026.

SNB remains prepared to sell FX

EUR/CHF has edged higher today after the SNB avoided the more aggressive 50bp rate hike option. However, this exchange rate remains heavily managed by the SNB and we doubt it will embark on a major rally just yet.

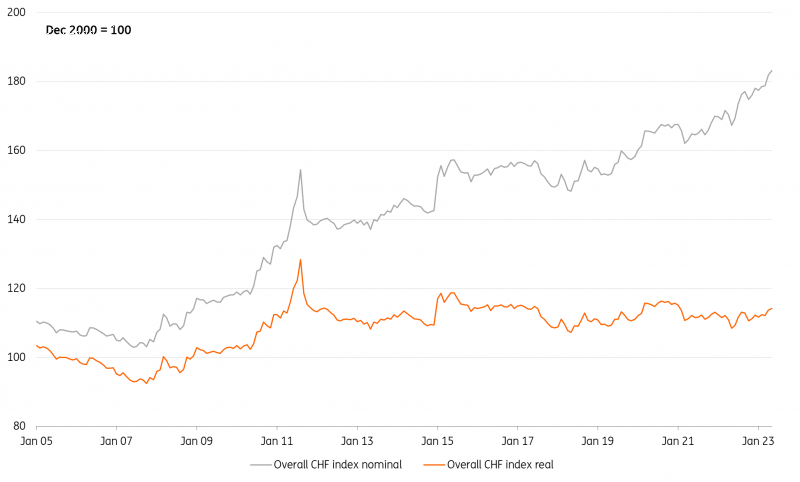

In today’s press conference, the SNB said that it had been selling FX over recent quarters. This is consistent with its policy – elaborated upon last year – that it wanted to keep the real Swiss franc stable to fight inflation.

As you can see from the chart below, the SNB has been effective in keeping the real exchange rate stable. To deliver real exchange rate stability it has allowed/engineered a 2% nominal appreciation of the trade-weighted Swiss franc over the last quarter.

With the inflation differential between Switzerland and its main trading partners (the eurozone and the US) expected to narrow over the coming quarters and following years, the SNB will presumably not have to engineer quite as much nominal appreciation to keep the real CHF stable.

If we are right with our forecast for a weaker dollar over the next 12 months, it looks like a lower USD/CHF will do the heavy lifting for the modest gains in the nominal CHF, needed to keep the real exchange rate stable. This means that EUR/CHF will probably continue to trade in a 0.97-0.99 range for most of this year and will only be allowed by the SNB to trade substantially higher if USD/CHF falls even harder.

The SNB has been effective in keeping the real exchange rate stable

source: ING

Leave a Reply

You must be logged in to post a comment.