Weekly Forex Analysis

Global markets have finally caught their breath after the longest U.S. government shutdown on record, but uncertainty continues to dominate sentiment. As traders await a revised data-release schedule from the BLS, the week ahead is packed with inflation reports from Canada, Japan, and the United Kingdom, with attention firmly on central bank policy signals. Meanwhile, the lack of October U.S. data keeps many currency trajectories clouded in ambiguity.

Summary

The past week began with the announcement that the U.S. government had reopened, but elevated volatility and risk-averse sentiment remained firmly in place. Uncertainty over delayed releases—such as September NFP and key inflation data—has left traders essentially “driving through fog.” Elsewhere, inflation readings from Japan, New Zealand, Canada, and the U.K. will be in focus, as they could further clarify central bank policy direction. In this environment, the U.S. Dollar is expected to stabilize, the Pound faces pressure from rate-cut expectations, and the Canadian Dollar is entering a crucial week dominated by CPI and retail data.

Key Points

- The end of the 43-day U.S. government shutdown has revived expectations for gradual release of delayed economic data.

- September NFP may be released this week, although October data may never be recovered.

- Canada’s CPI, Japan’s inflation data, and U.K. CPI are the top macro drivers of the week.

- Market confidence is returning slowly but remains fragile, and volatility is still elevated.

- Flash PMIs from Europe, the U.S., and the U.K. will help gauge global economic activity.

- The British Pound is under strong pressure due to rising expectations of a BoE rate cut.

- The Canadian Dollar faces a pivotal week with CPI and housing data.

- The Japanese Yen is caught between inflation above 2% and a hesitant central bank.

- The U.S. Dollar is expected to enter a phase of stabilization rather than continuation of its previous trend.

Review of Last Week

The previous week opened with optimism following the end of the 43-day U.S. government shutdown. Equity markets initially reacted positively, but the optimism didn’t last long. Sudden swings and unexplained selloffs made it clear that investors still lack confidence in the global economic outlook.

U.S. Government Shutdown Impact

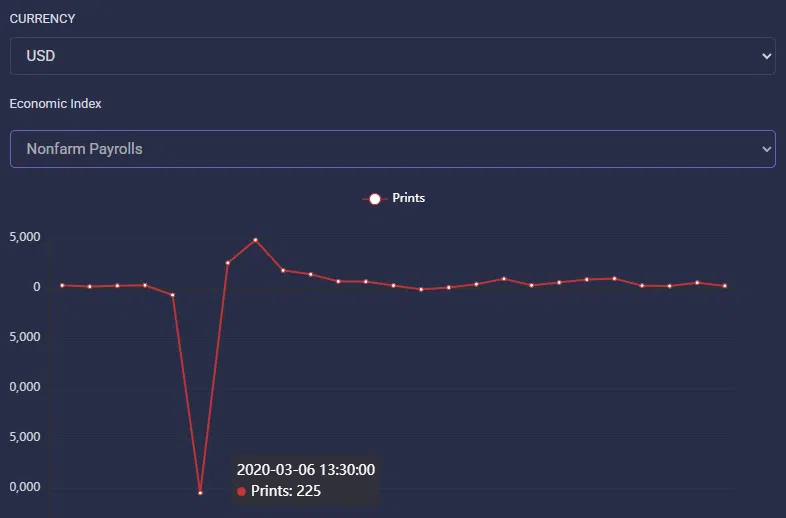

One of the biggest sources of anxiety was the absence of critical U.S. economic data. Private-sector indicators such as the new ADP weekly series showed an average loss of 11,000 jobs over the past four weeks, deepening concerns. Adding fuel to the fire, the White House spokesperson suggested that October data “may never be recovered,” amplifying uncertainty.

Crypto Market

The crypto market struggled again, with significant capital outflows. Total market capitalization declined nearly 10%, while other risk assets—despite sharp swings—mostly rebalanced toward previous averages.

Asia-Pacific Developments

Weak Chinese trade data drew strong attention across Asia. Meanwhile, Japan prepared for GDP and CPI releases, with traders watching closely for clues on the Bank of Japan’s future policy stance.

Overall, last week reflected a mix of government reopening, data-related anxiety, and elevated volatility—setting the stage for a decisive week ahead.

Market Outlook and the Week Ahead

The coming week holds special significance for global markets as traders anticipate the first indications of a revised U.S. data-release schedule. Attention is centered on how the BLS intends to recover missing data, especially September NFP, PCE updates, and retail sales.

At the same time, a wave of inflation data from Canada, the U.K., and Japan may shift expectations surrounding upcoming rate decisions. Meanwhile, Flash PMIs across the U.S. and Europe will offer real-time insight into the state of global economic activity.

For forex traders, the week ahead blends uncertainty, sensitive data releases, and evolving central-bank signals—creating a complex yet opportunity-rich environment.

Major Drivers of the Week

The foreign-exchange market will navigate a combination of key macro events: gradual reintroduction of U.S. data, inflation releases from three major economies, and forward-looking indicators such as PMIs. Investors are caught between missing U.S. data and the policy cues that central banks may deliver as the year approaches its final stretch.

United States — The Most Important Catalyst

From the U.S., the biggest potential market-moving event is the possible release of September NFP and a new roadmap from the BLS. The unclear fate of October data remains a major obstacle for forecasting the interest-rate path, as neither CPI nor employment data for October are available. As Fed Chair Jerome Powell described, policymakers are essentially “driving through fog.”

Europe

Flash PMIs will be crucial in the Eurozone. While recent data suggests tentative stabilization, the manufacturing sector remains weak, and service-sector momentum is soft. The PMI trajectory will likely determine short-term sentiment on the Euro.

UK CPI

In the U.K., October CPI is the highlight. A renewed drop in inflation would further solidify market expectations of a December rate cut by the Bank of England. This would likely weigh on the Pound unless retail sales or PMI surprises provide support.

Canada enters a data-heavy week with CPI, retail sales, and housing reports. Meanwhile, in Japan, inflation data, trade balance, and machinery orders will shape expectations for future BoJ tightening.

Key speeches by central-bank officials—including the SNB—may also add bursts of intraday volatility.

Overall, the week stands out as one of the most sensitive periods of the year, driven by inflation themes, forward-looking data, and waning U.S. uncertainty.

Currency Outlook

Below is a currency-by-currency breakdown based on the analysis of the three preparatory articles you provided.

🇺🇸 US Dollar (USD)

The U.S. Dollar has shifted into a “stabilization phase” after weeks of conflicting private-sector signals and missing official data. Hopes for a gradual release of delayed figures support the Dollar, but missing October numbers remain a major limitation.

If September NFP, housing data, or PMIs outperform expectations, the Dollar may pivot from stabilization toward strength. However, weak PMIs or disappointing private-sector signals could revive recessionary concerns and pressure the currency.

Weekly Bias: Stabilizing, with upside risk if data surprises to the upside.

🇪🇺 Euro (EUR)

The Euro attempted to build momentum last week on the back of mildly improving regional data. Better-than-expected GDP and signs of stabilization in PMIs strengthened expectations that the ECB may pause rate cuts.

This week, European Flash PMIs and final October CPI will be key. A return of PMIs toward or above 50 would support the Euro, while renewed weakness could reawaken recession fears.

Weekly Bias: Slightly bullish, data-dependent.

🇬🇧 British Pound (GBP)

The Pound is one of the most vulnerable currencies this week. Recent CPI data was less alarming than feared, yet traders still price an ~80% probability of a December rate cut.

With October CPI, retail sales, and Flash PMIs all due, the Pound faces volatility. Another drop in inflation would likely push GBP lower, unless consumption and business activity data offset the weakness.

Weekly Bias: Bearish-leaning, highly dependent on CPI.

🇯🇵 Japanese Yen (JPY)

The Yen remains stuck in a complex environment. Inflation remains above 2%, but the BoJ remains ultra-cautious, and political pressure to support growth has increased.

With GDP, CPI, trade data, and machinery orders all scheduled, the Yen has numerous catalysts. A hotter CPI print could boost expectations for eventual rate hikes or at least a more hawkish BoJ tone.

Weekly Bias: Mildly bullish, with strong domestic catalysts.

🇨🇦 Canadian Dollar (CAD)

The Canadian Dollar enters a highly data-sensitive week. October CPI is the most important release, although housing and retail-sales data also carry weight.

Forecasts point to a moderation in headline inflation. A softer-than-expected CPI would likely weaken CAD as markets assume the BoC is near the end of its tightening cycle.

Weekly Bias: Bearish unless CPI beats expectations.

🇦🇺 Australian Dollar (AUD)

The AUD faces several catalysts: RBA meeting minutes and the Wage Price Index (WPI). Wage growth is expected to remain elevated, which could delay rate-cut expectations.

Despite solid employment figures last week, uncertainty remains high due to weak Chinese trade data and sluggish local momentum.

Weekly Bias: Neutral to slightly bearish unless WPI is strong.

🇳🇿 New Zealand Dollar (NZD)

New Zealand will release PPI and trade-balance data. Higher production inflation could rekindle expectations of policy tightening by the RBNZ, while weak trade results would weigh on NZD.

The market is watching closely for any signs of policy shifts.

Weekly Bias: Bearish-leaning, sensitive to production and trade data.

Upcoming Economic Calendar

Monday – 17 Nov 2025

CAD – CPI

CAD – Housing Starts

CAD – Home Resales

JPY – Q3 GDP (preliminary)

USD – NY Fed Manufacturing Index

Tuesday – 18 Nov 2025

AUD – RBA Meeting Minutes

AUD – Wage Price Index

NZD – Producer GDP (PPI)

USD – ADP Weekly Employment

Wednesday – 19 Nov 2025

CNY – PBoC Rate Decision

EUR – Eurozone Core CPI (HICP)

JPY – Machinery Orders

JPY – Trade Balance

USD – Housing Starts

USD – Building Permits

Thursday – 20 Nov 2025

JPY – National CPI

NZD – Trade Balance

USD – Potential September NFP (BLS)

USD – Philadelphia Fed Index

GBP – U.K. CPI

Friday – 21 Nov 2025

GBP – Retail Sales

GBP – Flash PMIs

EUR – Flash PMIs

USD – Flash PMIs

USD – Michigan Consumer Sentiment

CHF – SNB Chairman Jordan Speech

Final Notes & Risk Disclosure

The week ahead presents one of the most data-intensive and uncertain environments in recent months. While the U.S. government reopening offers hope for missing data to gradually return, the absence of October numbers still clouds visibility on the Fed’s outlook. Meanwhile, inflation prints from Canada, Japan, and the U.K. will directly influence market expectations for upcoming rate decisions.

Traders should remain aware that sudden volatility is possible as markets adjust to new information and unpredictable release schedules. Risk management and position sizing are essential in such conditions.

⚠️ All analysis above is based on currently available information and may shift once new data is released or prior releases are revised. Forex trading carries inherent risk, and each trader should act according to their own strategy and risk-management rules.