In this week’s Forex market analysis, the central focus revolves around a single key concept: validation. Following the Federal Reserve’s recent decision, markets have entered a new week where the overall environment remains risk-friendly and constructive. However, this optimism is entirely conditional on confirmation from upcoming U.S. inflation and labor market data. The easing of financial conditions in the United States has supported risk assets, precious metals, and higher-yielding currencies, but market conviction about the durability of this trend depends on data, not promises.

For Forex traders, the week ahead is less about directional trading and more about a confrontation between competing narratives. Monetary policy divergence among major central banks remains the dominant force shaping price action, while sensitivity to data, particularly U.S. NFP and CPI figures, has increased noticeably. This article aims to provide a clearer framework for decision-making in the coming week by reviewing last week’s developments, assessing current market conditions, and identifying the key macroeconomic drivers.

Key Takeaways

- The overall market environment is risk-on, but this stance remains entirely data-dependent.

- The U.S. dollar is less a reflection of growth and more a pricing mechanism for Federal Reserve policy expectations.

- Monetary policy divergence remains the primary driver of currency pairs in the week ahead.

- High-yielding and carry currencies are currently more attractive than defensive currencies.

- The Japanese yen continues to function as the market’s funding currency, but short-squeeze risks are elevated.

- Trading focus should remain on relative value trades and intelligent pair selection, rather than chasing emotional price moves.

Previous Week

Last week was dominated by the highly anticipated Federal Reserve decision. The 25-basis-point rate cut marked a formal end to the era of interest rates above 4 percent, a move that markets had priced in well in advance. However, what mattered more than the rate cut itself was the combination of messaging, the dot plot, and the tone of Jerome Powell’s press conference. At first glance, the decision could have been interpreted as hawkish given the limited number of projected cuts next year, yet the market drew a different conclusion.

The U.S. dollar weakened notably following the meeting. Rather than focusing on the number of cuts signaled, traders concentrated on the Fed’s indirect messages, references to a gradual cooling in the labor market, uncertainty surrounding employment data, and the need to preserve liquidity in financial markets. The announcement of short-term Treasury purchases was also interpreted as supportive of financial conditions, further adding to downward pressure on the dollar.

Across asset markets, the picture was mixed. The Dow Jones Industrial Average posted new all-time highs, while the Nasdaq came under pressure due to capital rotation from technology stocks into more traditional sectors. Precious metals, particularly silver, experienced significant gains, although part of this rally was later met with profit-taking. Overall, last week reaffirmed that the “currency debasement trade” has re-emerged, but it also highlighted that the market has entered a more sensitive phase, one in which the sustainability of this narrative is being actively tested. Attention has now fully shifted to the week ahead.

Market Update and the Week Ahead

The upcoming week is shaping up to be one of the busiest and most decisive periods in recent months for the Forex market. The return of key U.S. data, combined with policy decisions from four major central banks, creates an environment in which each data point carries more weight than usual. Following the Federal Reserve’s rate cut, markets are no longer trading assumptions; they are demanding evidence.

The core question is whether incoming data can validate the narrative of gradual easing without a resurgence in inflation. If confirmed, risk-sensitive and carry currencies are likely to remain supported. However, if the data points to renewed inflationary pressures or persistent wage growth, markets may be forced to recalibrate expectations. This environment sets the stage for targeted volatility and selective opportunities in currency markets.

Key Catalysts for the Week Ahead

The most important drivers this week are U.S. labor market and inflation data. The delayed release of the November NFP report, alongside CPI data, will directly influence expectations for future Federal Reserve rate moves. Signs of further weakness in the labor market could reinforce expectations for additional rate cuts, while any upside surprise in wages or inflation would revive concerns about a pause or slowdown in the easing cycle.

Beyond the United States, policy decisions from the European Central Bank, the Bank of England, and the Bank of Japan will also play a critical role. The Bank of England faces a market that has largely priced in a rate cut, with attention focused on the tone of its statement and its outlook for 2026. The ECB is expected to leave rates unchanged, but a renewed emphasis on policy being in a “good place” could offer support to the euro. In Japan, expectations for a rate hike have increased, yet markets are more sensitive to forward guidance and signals about the policy path for the coming year than to the decision itself.

Overall, the week ahead is not about headline-grabbing decisions, but about precise interpretation of data and messaging. The market is prepared to react, but confidence remains fragile.

Currency Outlook for the Week Ahead

🇺🇸 United States Dollar (USD)

The U.S. dollar continues to trade less as a reflection of economic growth and more as a mirror of Federal Reserve policy expectations. Following the rate cut and Powell’s less-hawkish-than-expected tone, financial conditions in the United States have eased, placing structural pressure on the dollar. Markets are currently keeping the scenario of further rate cuts alive, and any data that supports this narrative is likely to result in additional dollar weakness.

In the coming week, NFP and CPI data will be decisive. If employment data signals further labor market softening and inflation remains contained, the dollar is likely to stay under pressure against higher-yielding currencies and those with more stable policy outlooks. Conversely, an upside surprise in wages or inflation could temporarily halt dollar selling and force a partial reassessment of market expectations. Nevertheless, in the near term, the prevailing bias remains toward a controlled weakening of the dollar.

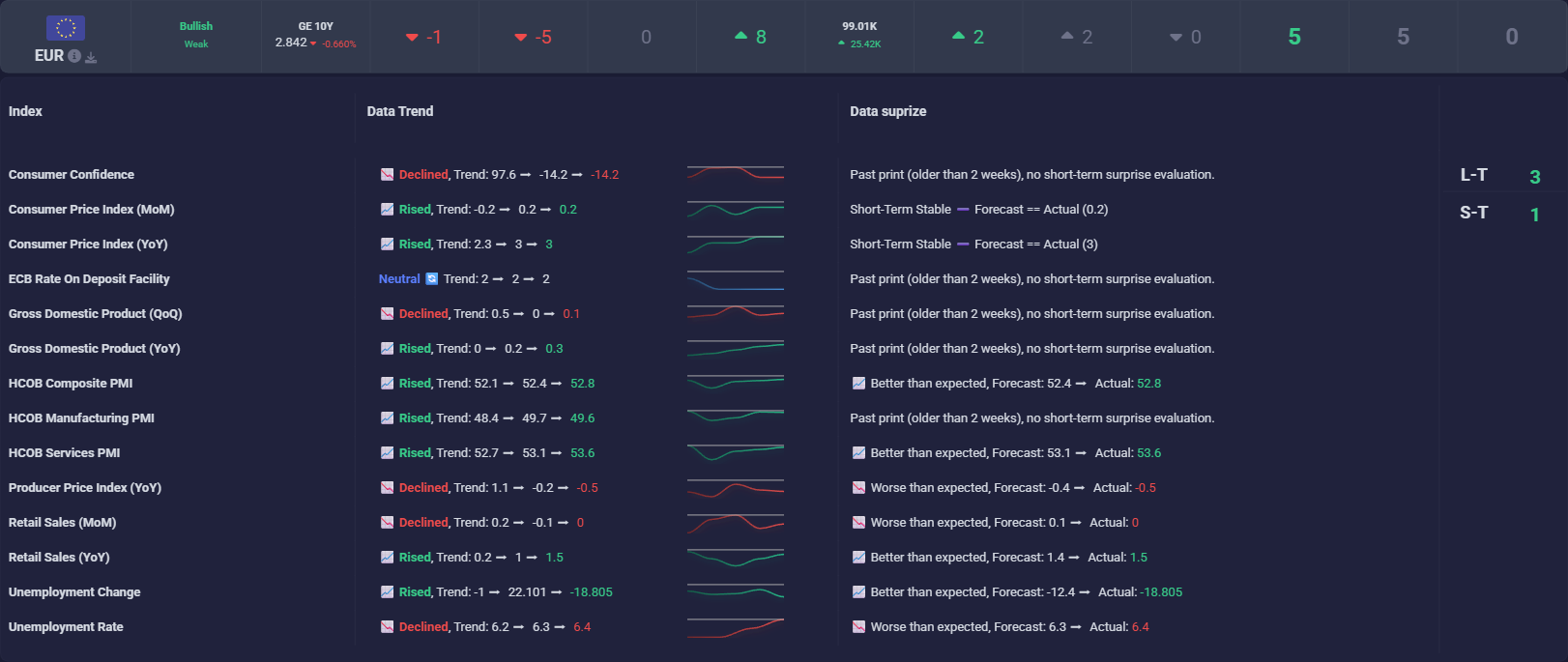

🇪🇺 Euro (EUR)

The euro enters the week supported by ECB policy stability and a modest improvement in sentiment surrounding the euro area economy. Repeated emphasis by ECB officials that policy is in a “good place,” along with comments hinting at a potential upward revision to growth expectations, has underpinned the currency.

In the base case, policy stability in Europe combined with dollar weakness should work in the euro’s favor, particularly if PMI data suggests a more resilient economic backdrop. The primary risk for the euro would be a negative growth shock or a renewed escalation of trade concerns that reactivates discussions around further policy easing. Overall, the euro’s short-term outlook is assessed as relatively constructive, especially against the dollar and the pound.

🇯🇵 Japanese Yen (JPY)

The Japanese yen remains one of the most distinctive currencies in the market, simultaneously the weakest in terms of performance and the most dangerous from a short-squeeze risk perspective. Despite rising expectations for a Bank of Japan rate hike, the yen has failed to capitalize meaningfully and continues to serve as the primary funding currency for carry trades.

This week, the Bank of Japan’s decision and, more importantly, its forward guidance are of critical importance. If a rate hike is accompanied by cautious messaging about the path ahead, selling pressure on the yen may persist. However, any stronger signal regarding continued tightening, or a spike in global market volatility, could trigger a rapid unwinding of short positions. As such, while the dominant trend for the yen remains fragile, the risk of sudden upside moves should not be underestimated.

🇬🇧 British Pound (GBP)

The British pound is positioned as one of the more vulnerable major currencies on a relative basis. Weak growth momentum, signs of labor market cooling, and strong market expectations for rate cuts have all weighed on sterling. A Bank of England rate cut in the coming week is widely seen as a near certainty, with market focus firmly on the tone of the statement and the outlook for 2026.

If the rate cut is accompanied by dovish guidance and inflation data continues to soften, the pound could face additional pressure. The only scenario that could offer support would involve stronger-than-expected domestic data or a more cautious stance from the central bank regarding the pace of future easing. Overall, sterling is likely to remain on the defensive, particularly against carry currencies and the euro.

🇨🇦 Canadian Dollar (CAD)

The Canadian dollar continues to lack a strong independent catalyst and is trading largely as a reflection of broader risk sentiment and external developments. Monetary policy remains in a wait-and-see mode, and oil prices have failed to generate a clear directional impulse. In such an environment, the CAD tends to deliver middle-of-the-road performance.

Inflation data this week could trigger short-term volatility, but it is unlikely to alter the broader trend. In a risk-on scenario, the Canadian dollar may perform reasonably well, but it remains less attractive than currencies such as the Australian and New Zealand dollars. Overall, the outlook for the CAD is characterized by range-bound and uneven price action.

🇨🇭 Swiss Franc (CHF)

In the current market environment, the Swiss franc has gradually lost some of its defensive appeal. Improved risk sentiment and an unfavorable yield differential have reduced investor appetite for holding CHF. Unless a geopolitical shock or a sharp risk-off episode emerges, the franc is likely to underperform against cyclical and carry currencies.

🇦🇺 Australian Dollar (AUD) and 🇳🇿 New Zealand Dollar (NZD)

The Australian and New Zealand dollars are among the clearest beneficiaries of the current market environment. Policy stability, attractive yields, and improving global risk sentiment have positioned these currencies as favored carry trade candidates. In the absence of negative data shocks, both are expected to outperform low-yielding currencies such as the yen, Swiss franc, and pound. The short-term outlook for both currencies remains constructive.

Economic Calendar Ahead

Monday

🇨🇦 CAD – Canadian inflation data

Tuesday

🇺🇸 USD – NFP employment report

🇬🇧 GBP – UK employment data

🇪🇺 EUR – Flash PMIs

Wednesday

🇺🇸 USD – U.S. retail sales

🇬🇧 GBP – UK inflation data

Thursday

🇺🇸 USD – U.S. CPI

🇬🇧 GBP – Bank of England rate decision

🇪🇺 EUR – ECB monetary policy decision

Friday

🇯🇵 JPY – Bank of Japan rate decision

Notes

The week ahead is, above all, a test of market confidence. Markets have priced in a scenario of gradual easing without a return of inflation, but this scenario remains fragile and dependent on data confirmation. In such an environment, relative value trades, careful currency pair selection, and disciplined risk management take precedence over aggressive directional positioning.

Professional traders are likely to focus on carry currencies, policy divergence, and market reactions to key data releases. This week may define short-term direction, but more importantly, it will shape the market’s sensitivity to data in the weeks ahead.

Risk Disclosure: The Forex market inherently involves high risk, and volatility driven by economic data and central bank decisions can lead to significant losses. This analysis is provided for educational and informational purposes only and should not be construed as investment advice. All trading decisions are the sole responsibility of the trader.