This weekly Forex Analysis centers on the highly anticipated Federal Reserve meeting and its decision regarding the continuation of the rate-cutting path. Markets are almost certain that a 25-basis-point reduction will be announced, yet the real significance lies in the tone of the statement, the details of economic forecasts, and the outlook for 2026. Investors currently face critical questions: Will the Fed deliver a cautious message, or leave the door open for further cuts? Each scenario could profoundly affect currencies, including the US dollar, euro, antipodean currencies, the yen, and the Swiss franc.

In this article, we provide a comprehensive overview of market conditions, review last week’s performance, and then move into the upcoming week’s main drivers. The most critical part of the analysis—the currency outlook—is developed using a fully fundamental approach and draws from the data of three reference reports, allowing traders to gauge potential paths for each currency under different scenarios. This analysis will help you identify which currencies are strong, which are exposed to risk, and how central bank policies may shift capital flows.

Key Points

- Market expectations for a 25-basis-point Fed rate cut are high, supporting risk appetite.

- Upcoming meetings of the RBA, BoC, and SNB are unlikely to result in sudden policy changes.

- The US dollar remains under pressure, while the euro and antipodeans (AUD and NZD) are performing better.

- Gold and oil remain sensitive to geopolitical developments, particularly the Ukraine-Russia negotiations.

- Japan’s policy stance and potential BoJ rate hikes are likely to influence yen volatility.

Review of Last Week

Last week, global financial markets experienced a mild risk-on sentiment. Rising expectations for Fed rate cuts helped US indices stabilize in positive territory. Employment data falling below expectations further strengthened these expectations. Consequently, traders increasingly priced in a 25-basis-point rate cut at the upcoming FOMC meeting.

In the currency market, the US dollar softened slightly, stabilizing around 98.9 on the DXY. The euro performed relatively well, reaching 1.1651, while the Japanese yen remained near 155 JPY per USD, influenced by anticipated BoJ rate hikes. The Canadian dollar recorded its strongest six-month gain versus the dollar, and the British pound traded near 1.335, close to a six-week high.

Overall volatility remained modest, yet the market felt like “the calm before the storm” as all eyes focused on the Fed meeting. As we move into the new week, the direction of currencies and risk assets will hinge heavily on the outcomes of this pivotal event.

Market Update and the Week Ahead

A clear focus dominates the coming week in Forex: the Fed’s decision and its 2026 policy outlook. While a 25-basis-point cut is largely expected, the significance lies in the “why” and “how” of this decision. Powell’s tone, the committee’s assessment of employment and inflation, and the reflection of these factors in the 2026 outlook will determine whether global markets remain risk-on or face renewed caution.

US Rates and Market Expectations

Downward pressure on the dollar remains evident, while some currencies, including the euro, Australian dollar, and New Zealand dollar, hold relative strength. Last week’s capital flows show that, after months of focusing on US inflation data, traders are now turning their attention to central bank direction in early 2026. This evolving environment can create vastly different scenarios for each currency, making the forthcoming currency outlook one of the week’s most critical analysis components.

Key Market Drivers This Week

Several key drivers could change market direction and create very different scenarios for traders:

1. Federal Reserve Decision and Economic Forecasts

The most important event is the Fed meeting. Markets expect a 25-basis-point rate cut, but key questions include:

- Will Powell present the cut as “cautious”?

- Will the Fed remain strict on 2026 inflation projections?

- Is there a possibility of further cuts in early 2026?

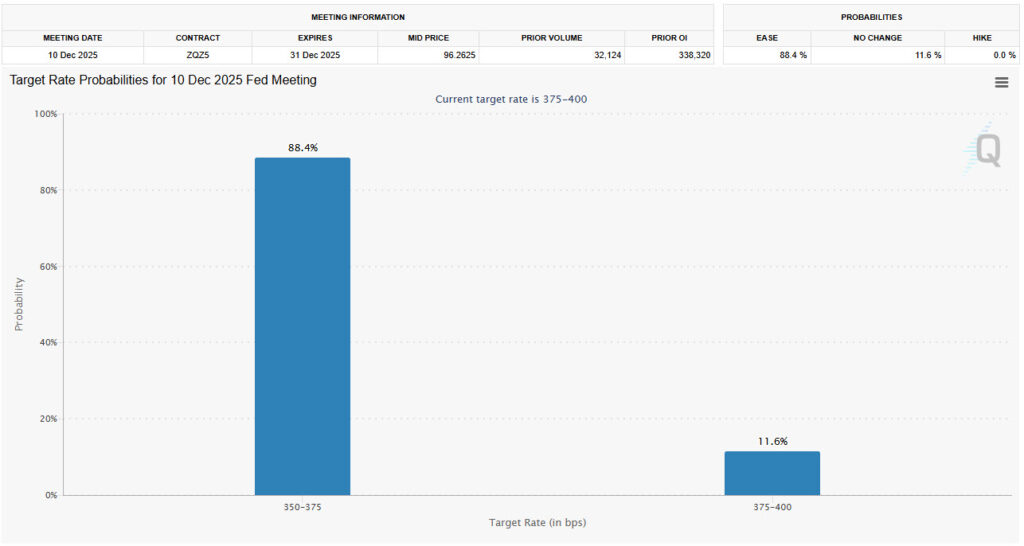

Powell’s tone could decisively shape dollar direction and capital flows. Current probability for a Fed rate cut on December 10, 2025, stands at 88.4%.

2. RBA, BoC, and SNB Decisions

The Reserve Bank of Australia is likely to maintain its current rate, despite persistently high inflation. The Bank of Canada, after several cuts, appears set for a temporary pause. The Swiss National Bank, facing very low inflation, is expected to maintain its policy. While not as pivotal as the Fed, these decisions will significantly impact AUD, CAD, and CHF.

3. BoJ Expectations

Markets are closely watching any guidance from the Bank of Japan regarding rate hikes. An implicit approval of higher rates could trigger substantial yen volatility.

4. US Inflation and Employment Data

Core PCE, jobless claims, and other releases will complement Fed messaging, offering a comprehensive picture of US economic health.

5. Geopolitical Developments and Commodities

Oil and gold remain highly sensitive to Ukraine-Russia negotiations. Any progress or setbacks could cause sudden shifts.

Currency Outlook This Week

🇺🇸 US Dollar (USD)

The Fed remains the central focus for the dollar. Markets have priced in a 25-basis-point cut, creating downward pressure. November employment and inflation data were soft enough to support this scenario. However, the key factor is the 2026 outlook: whether the pace of cuts continues or halts.

A cautious Fed tone emphasizing data dependence could stabilize or slightly strengthen the dollar. Conversely, hints of further cuts would boost risk appetite, weakening the dollar versus EUR, AUD, and NZD. Better-than-expected US data could push the dollar up, while weaker data would reinforce the downtrend.

🇪🇺 Euro (EUR)

The euro benefits from ECB policy stability and the gradual US rate cuts, narrowing rate differentials. Last week, EUR/USD performed well as markets recognized ECB’s measured approach. Strong German industrial data would further support euro strength. A dovish Fed could attract more capital into the euro, while a more hawkish tone or slower 2026 cuts might trigger a correction.

🇯🇵 Japanese Yen (JPY)

The yen faces a tug-of-war between potential BoJ rate hikes and its role as a funding currency in risk-on periods. Recent reports indicate Japan is seriously considering rate increases, which partly strengthened the yen last week. However, slow hike pace and yield differentials with the US remain limiting factors. Risk-on scenarios post-FOMC may pressure the yen, while aggressive Fed signals could lead to rapid yen gains. It remains attractive for hedging this week.

🇬🇧 British Pound (GBP)

Structurally weaker, the pound faces underwhelming economic data in services and housing. Markets are pricing in a BoE rate cut, keeping GBP behind EUR and antipodeans. Strong UK GDP could ease pressure slightly, but weak data would likely see GBP fall most against EUR and AUD.

🇨🇦 Canadian Dollar (CAD)

Following strong employment data, CAD recorded its best six-month performance. However, BoC is expected to hold rates, leaning slightly cautious due to domestic economic conditions and trade uncertainties. A dovish Fed could lift CAD slightly, but it remains weaker than AUD and NZD. Weak Canadian data or risk-off sentiment may trigger corrections.

🇨🇭 Swiss Franc (CHF)

CHF remains under pressure in a risk-on environment. SNB faces very low inflation and is unlikely to cut rates, maintaining a stable policy. CHF could strengthen only if a hawkish Fed triggers negative market reactions; otherwise, the downward trend continues.

🇦🇺 Australian Dollar (AUD)

AUD is one of this week’s most attractive currencies. RBA has paused after three cuts, with inflation pressures stabilizing. A dovish Fed could make AUD a top performer. Strong Chinese data would further amplify gains. Only aggressive Fed messaging or weak Chinese figures could weaken AUD.

🇳🇿 New Zealand Dollar (NZD)

NZD similarly benefits from stable RBNZ policy and global risk appetite. A dovish Fed could lift NZD further, while risk-off conditions or hawkish FOMC messaging could trigger a short-term correction.

Economic Calendar

Tuesday, December 9, 2025

- USD – Fed rate decision

- AUD – RBA rate announcement

- CAD – BoC rate decision

Wednesday, December 10, 2025

- CHF – SNB policy decision

- JPY – BoJ monetary policy decision

Thursday, December 11, 2025

- USD – Core PCE

- USD – Jobless claims

Friday, December 12, 2025

- GBP – Monthly GDP

- GBP – Services PMI

Final Notes

The coming week is among the most pivotal for currency trends in the months ahead. The Fed’s decision and its presentation will influence not only the dollar but global capital flows. Currencies like AUD, NZD, and EUR are positioned to attract investment, while GBP and CHF remain under pressure. The Japanese yen sits at a critical juncture between new policy directions and market risk sentiment.

Professional traders should closely monitor key data and initial market reactions. Scenarios can shift rapidly, making flexibility and robust risk management essential.

⚠️ Risk Disclosure Forex trading carries a high risk of capital loss. Sudden changes in central bank policies, economic data, or geopolitical events may lead to extreme volatility. Risk management and setting stop-loss levels are strongly recommended.