March 30, 2023

Swiss authorities and UBS bank are trying to close the deal with Credit Suisse by the end of April

Swiss authorities and UBS bank are trying to close the deal with Credit Suisse by the end of April

Ali Sabbaghi

0

Swiss authorities and UBS bank are trying to close the deal with Credit Suisse by the end of April

Bitcoin’s hash rate is now 3 times when Bitcoin was 60 thousand dollars!

It could be a positive sign for bitcoin and altcoins

German headline inflation dropped in March to the lowest level since last summer. However, there are still no signs of any broader disinflationary trend outside energy and commodity prices

Has the disinflationary process started? We don’t think so. German March headline inflation came in at 7.4% Year-on-Year, from 8.7% YoY in February. The HICP measure came in at 7.8% YoY, from 9.3% in February. The sharp drop in headline inflation is mainly the result of negative base effects from energy prices, which surged in March last year when the war in Ukraine started. Underlying inflationary pressures, however, remain high and the fact that the month-on-month change in headline inflation was clearly above historical averages for March, there are no reasons to cheer.

Today’s sharp drop in headline inflation will support all those who have always been advocating that the inflation surge in the entire eurozone is mainly a long but transitory energy price shock. If you believe this argument, today’s drop in headline inflation is the start of a longer disinflationary trend. As much as we sympathised with this view one or two years ago, inflation has, in the meantime, also become a demand-side issue, which has spread across the entire economy. The pass-through of higher input prices, though cooling in recent months, is still in full swing. Widening profit margins and wage increases are also fueling underlying inflationary pressure, not only in Germany but in the entire eurozone.

Available German regional components suggest that core inflation remains high. While energy price inflation continued to come down and was even negative for heating oil and fuel, food price inflation continued to increase. Inflation in most other components remained broadly unchanged. Given that energy consumption is more sensitive to price changes than food consumption, it currently makes more sense for the European Central Bank to only look at headline inflation that excludes energy but includes food prices when assessing underlying inflationary pressure.

All this means is that just looking at the headline number is currently misleading; there are still few if any signs of any disinflationary process outside of energy and commodity prices.

Looking ahead, let’s not forget that inflation data in Germany and many other European countries this year will be surrounded by more statistical noise than usual, making it harder for the ECB to take this data at face value. Government intervention and interference, whether that’s temporary or permanent or has taken place this year or last, will blur the picture. In Germany, for example, the Bundesbank estimated that energy price caps and cheap public transportation tickets will lower average German inflation by 1.5 percentage points this year. And there is more. Negative base effects from last year’s energy relief package for the summer months should automatically push up headline inflation between June and August.

Beyond that statistical noise, the German and European inflation outlook is highly affected by two opposing drivers. Lower-than-expected energy prices due to the warm winter weather could are likely to push down headline inflation faster than recent forecasts suggest. On the other hand, there is still significant pipeline pressure stemming from energy and commodity inflation pass-through and increasingly widening corporate profit margins and higher wages.

Even if the pass-through slows down, core inflation will remain stubbornly high this year.

As long as the current banking crisis remains contained, the ECB will stick to the widely communicated distinction between using interest rates in the fight against inflation and liquidity measures plus other tools to tackle any financial instability. The fact that there are still no signs of any disinflationary process, discounting energy and commodity prices, as well as the fact that inflation has increasingly become demand-driven, will keep the ECB in tightening mode.

The turmoil of the last few weeks has been a clear reminder for the ECB that hiking interest rates, and particularly the most aggressive tightening cycle since the start of monetary union, comes at a cost. In fact, with any further rate hike, the risk that something breaks increases. This is why we expect the ECB to tread more carefully in the coming months. In fact, the ECB has probably already entered the final phase of its tightening cycle. It’s a phase that will be characterised by a genuine meeting-by-meeting approach and a slowdown in the pace, size and number of any further rate hikes.

We’re sticking to our view that the ECB will hike twice more – by 25bp each before the summer – and then move to a longer wait-and-see stance.

source: ING

Bank of England, Andrew Bailey BOE: Inflation is likely to come down sharply in the UK, it’s very high.

The economy is stronger than expected, but wages are weakening.

What monetary policy can and should do is to make sure that the inflation that has arrived from abroad does not turn into sustained inflation at home.

As we look at the inflation outlook today, we must be aware that the full impact of the higher bank rate has yet to be felt in financial markets and the real economy.

Sometimes, changes in supply can be as sudden and as important to the inflation outlook as changes in demand.

If swelling persists, additional contraction is required.

The MPC will base its decision on evidence as it emerges.

White House plans are still in flux. A House panel will examine SVB’s failure on Wednesday.

They are preparing to ask federal bank regulators to impose new rules on mid-sized banks in the wake of the Silicon Valley bank’s collapse earlier this month.

But the administration is unlikely to ask Congress anytime soon to repeal the deregulation law passed five years ago with bipartisan support.

The exact details of the White House’s recommendations are unclear, but they would try to restore rules for banks between $100 billion and $250 billion that were removed by Congress and the Federal Reserve during the Trump administration.

According to Day Zeit, Philip R. Lane, ECB Chief Economist and Member of the Executive Board, says that the tensions in the banking sector are subsiding.

This pair, CADJPY seems to change its direction to the long. retracement on lower prices could be a great opportunity to enter a new long position with a nice win rate ratio.

95.9 and 94.8 is our main support levels.

The trend is buy, Stoch, and RSI are in the overbought area so it helps to drop the prices to a lower area and we are waiting for it.

The People’s Bank of China has already cut its Required Reserve Ratio and has continued to pump liquidity into the money market over the past few days. Is this about global market volatility or is it more about the domestic economy?

China’s central bank, the PBoC, has injected significant liquidity into the market since 21 March. From the 21st to the 29th of the month, the central bank injected more than CNY850 billion of net liquidity into the financial system. This includes CNY352bn injected through daily open market operations and CNY500bn by lowering the Required Reserve Ratio (RRR) which took effect on 27 March.

We believe that there are at least two considerations behind these liquidity injections.

These operations are occurring at the end of the first quarter. In China, loan growth for the year is usually booked in the first three months. This is a seasonal phenomenon and pushes up interbank interest rates at the end of the first quarter. As the chart shows, the overnight SHIBOR touched 2.5% on 20 March. Therefore, we think that loan growth should continue to be very strong in March compared to 2022, even after the rapid growth in the first two months. If this is the main reason for the PBoC’s big liquidity injection, this should be seen as a positive sign for economic growth.

The volatility in global financial markets is not over; there may be some ups and downs ahead. China has a more open capital account than in the past and global events may have some impact on the Chinese market. As such, the PBoC may be cushioning any potential volatility. This is more of a precautionary measure and should not be over-interpreted.

The market is actively discussing that the PBoC will cut the 7D policy rate and the medium-term lending facility (MLF) rate, which are currently at 2.0% and 2.75%, respectively. The discussion has intensified, especially after the PBoC announced a cut in the RRR this month.

We do not see the need for China to lower interest rates. The economy is recovering at this time, although not as fast as the market expected though this is due more to the market’s overestimation of the speed of the rebound. External markets are weakening and export activity will be dampened. But China’s interest rate cuts will not help exports. Moreover, an excessively accommodative monetary policy may attract some unnecessary investments. As the economy recovers more quickly in the second half of the year, interest rate cuts could pose a risk of economic overheating.

source: ING

Another improvement in sentiment in the German economy as the Ifo index increased for the sixth month in a row in March. However, we fear that the latest financial turmoil will reach the real economy in the coming months.

In March, Germany’s most prominent leading indicator, the Ifo index, increased for the sixth month in a row, coming in at 93.3 from 91.1 in February. Lower wholesale gas prices and the reopening of the Chinese economy have boosted economic confidence. Both the current assessment and expectations component increased significantly.

The financial market turmoil of the last few weeks has not yet affected economic sentiment – at least not economic sentiment measured by company surveys. The latest economic sentiment indicators nicely illustrate that for now, financial market turmoil appears to be ringfenced and has not affected the real economy: while the ZEW index, filled in by financial analysts, dropped, PMIs and now the Ifo index increased. We are more careful, however, and remind everyone that the Ifo index can react with a delay of one to two months to unexpected events and financial market turmoil can clearly affect the real economy over time.

The German economy will continue its flirtation with recession. But what is more important: the ongoing war in Ukraine, ongoing structural changes, an ongoing energy transition and the impact of the most aggressive monetary policy tightening in decades are the main drivers of what looks like subdued growth for a longer while.

source: ING

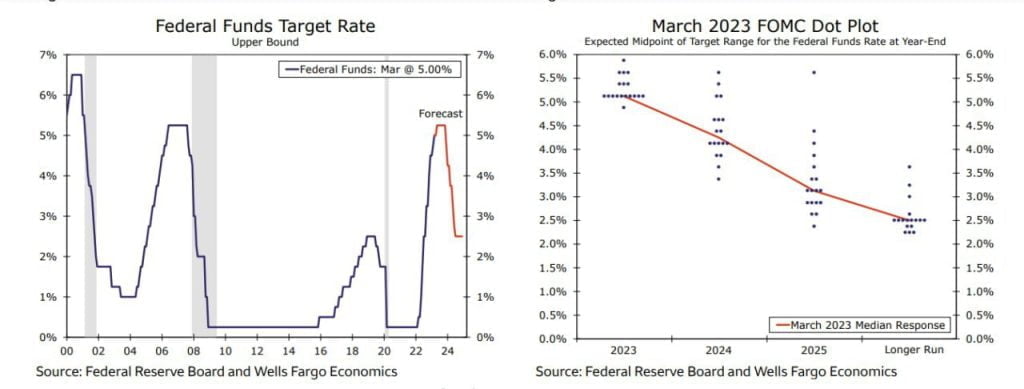

Wells Fargo Financial Institution: The Federal Reserve will increase interest rates, but the end of the monetary contraction cycle is coming!

The Federal Reserve increased its interest rate by 0.25% to 4.75-5%. Federal Reserve policymakers have raised interest rates by 4.75% over the past 12 months, the fastest rate of monetary tightening since the early 1980s. The Federal Reserve continued to maintain a relatively optimistic assessment of the current state of the economy. However, the central bank noted that recent developments will likely lead to tighter credit conditions and likely affect economic activity; Although the extent of these effects is unclear.

Previously, the Fed thought that a sustained increase in interest rates would be needed to bring inflation back to its 2 percent target, but now it thinks that some additional accommodative monetary policy may be in order. In short, the end of the Fed’s monetary tightening cycle appears to be coming. The median forecast for the terminal interest rate was only 0.25% higher than the previous forecast, and we expect the Fed to deliver another 0.25% rate hike at its next meeting.

Flow Trend

Flow Trend

Gold Extractor

Gold Extractor