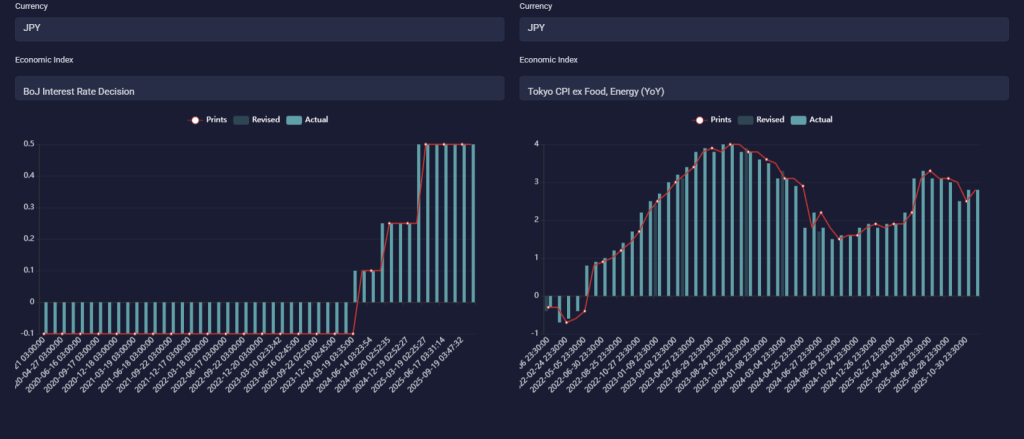

Last week, the Japanese Yen (JPY) rose more than half a percent against the US Dollar (USD), emerging as the best-performing currency in the G10 group. This remarkable rally followed comments from Bank of Japan Governor Ueda, which investors interpreted as a potential shift toward a tighter monetary policy. According to Scotiabank’s senior FX strategists, markets now expect a rate hike of around 21 basis points at the BoJ’s December 19 meeting, a significant revision from last week’s projections.

JPY Leading Global Markets

The 0.6% gain versus the USD is just part of the story. Investors reacted sharply to Governor Ueda’s statement that the BoJ would “consider the pros and cons of raising the policy rate.” This prompted the market to quickly revise expectations for a December rate increase. Short-term Japanese rates now price in a 21-basis-point hike, up from single-digit expectations just last week. This significant shift provides fundamental support for the Yen, with the 2-year US-Japan yield spread hitting a fresh low.

jpy-cpi-INTERESTRATE-JAPAN-1024×439

Global Market Developments

While the Yen strengthened, US equity markets finished slightly higher during a low-volume, post-Thanksgiving session. Major indices gained between 0.54% and 0.65%. In Europe, the EuroStoxx50 index recovered from early weakness to close 0.3% higher. These moves suggest the risk of a broad market sell-off has eased, at least temporarily.

US Treasury yields also edged higher, with the 10-year note breaking the 4% barrier. European markets remained relatively subdued. National inflation releases offered mixed signals: France and Italy fell short of expectations, while Spain and Germany slightly exceeded them. Nevertheless, these figures are unlikely to influence European Central Bank policy. ECB President Christine Lagarde noted last Friday that the 2% interest rate remains appropriate, highlighting that economic growth has already exceeded expectations.

UK Bond Market and Fiscal Policy

In the UK, short-term gilt yields saw a mild relief rally, while 30-year yields reached their lowest levels since June. The government’s recent budget provided some reassurance, increasing fiscal buffers and shifting toward more short-dated debt issuance. Despite these measures, long-term debt concerns remain, suggesting potential future market pressure. Meanwhile, the British Pound faces resistance against the Euro and the USD, with GBP/USD trading above 1.32.

Outlook for Japan

All eyes are on the BoJ’s December 19 meeting. Governor Ueda’s remarks about weighing the pros and cons of a rate hike, coupled with warnings about delaying the move, signal a potential hawkish shift. As a result, short-term Japanese yields rose 4–5 basis points, with the 2-year yield hitting 1% for the first time since 2008. These developments reinforce fundamental support for the Yen and may influence currency market volatility.

Other Global Economic Developments

Rating agency Moody’s confirmed Hungary’s credit rating at Baa2 with a negative outlook, citing slower growth and heavy reliance on the automotive sector and the German economy. Lower public investment and limited access to EU funds also weigh on growth, pushing the debt-to-GDP ratio slightly higher to around 74% for 2025 and 2026.

In oil markets, OPEC+ decided to pause production increases in Q1 2026 to stabilize supply and regain market share, boosting Brent crude prices to around $63.5 per barrel.

Conclusion

Overall, last week highlighted a strong Yen rally and a reassessment of BoJ policy expectations. These developments impact not only currency markets but also global equities and bond markets. Investors should closely monitor central bank announcements, inflation data, and fiscal changes, as these factors will continue to shape short- and medium-term market trends.