The week ahead places intense market attention on major US economic releases and expectations surrounding central bank decisions. The US dollar faces potential pressure from upcoming PMI, labor, and PCE inflation data, while the euro, pound, yen, and Antipodean currencies react to their respective domestic macro drivers. Precious metals and US equities continue to benefit from structural demand and hopes for near-term Fed easing. Traders will need to closely monitor risk sentiment, Federal Reserve guidance, global inflation trends, and geopolitical developments to position effectively through the week.

Key Points

- Markets remain focused on the probability of a Fed rate cut in December, but upcoming US data could shift expectations decisively.

- The US dollar is vulnerable to labor and inflation surprises and may face short-term downward pressure.

- The euro and pound remain supported by stable regional fundamentals and central bank policy stances.

- The yen continues to act as a funding currency with limited support unless a risk-off shock occurs.

- AUD and NZD are supported by investment strength and flexible domestic policies.

- Gold and silver remain well bid due to strong institutional demand and muted volatility.

- US equity indices continue to gain support from investor flows and confidence returning to AI and tech leadership.

Review of the Previous Week

Last week, markets were driven by a mix of economic readings and central bank communication. In the US, cooling inflation and mixed labor data strengthened expectations for a December rate cut. Equity markets and cryptocurrencies regained ground, erasing a significant portion of November’s losses. Thanksgiving holiday-driven low volumes suggest that many of these moves may be retested as normal liquidity returns.

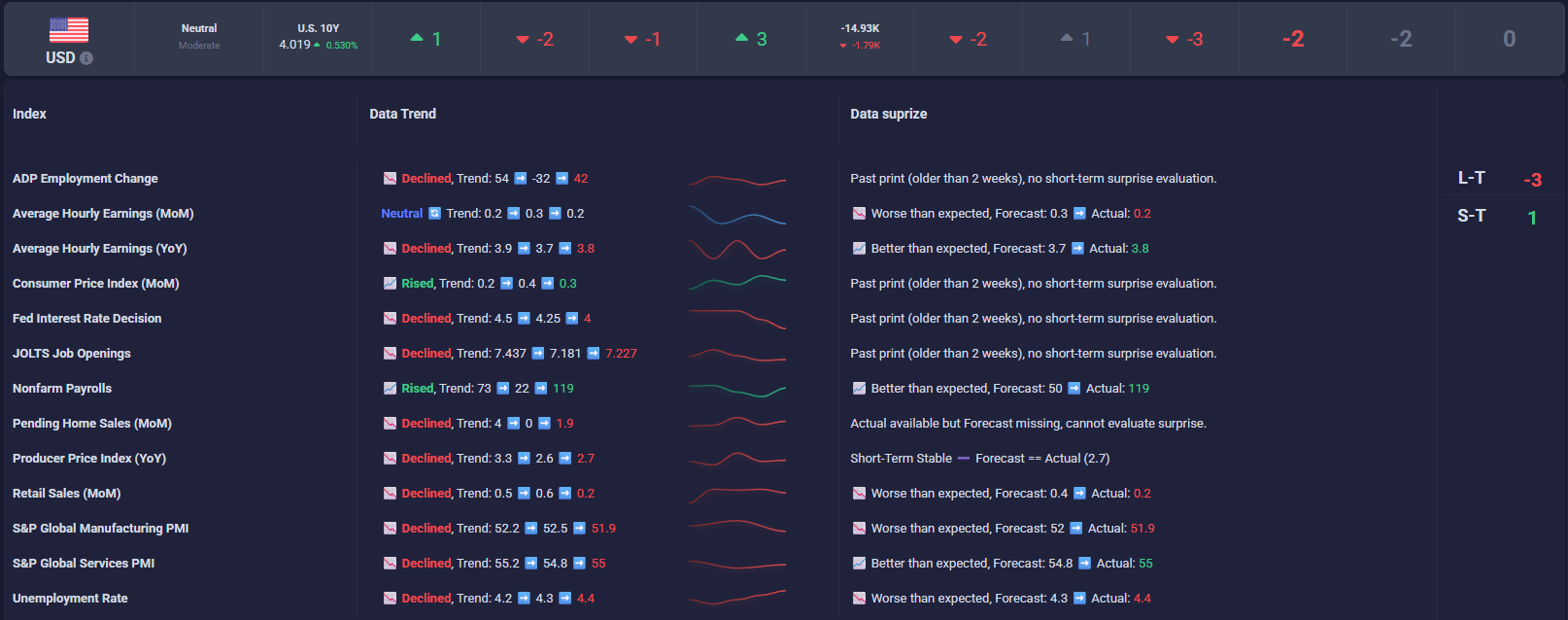

US economic data trend – 1 Dec 2025

In Europe, both the euro and the pound traded with relative stability, supported by a neutral-leaning ECB and a BoE preparing for an easing cycle. In Japan, the yen remained weak as the BoJ maintained its policy stance near the effective lower bound, and even hawkish commentary failed to generate sustained gains.

Australia and New Zealand experienced supportive flows as domestic inflation and investment data stabilized. Meanwhile, gold and silver approached new cycle highs, and US equities recorded a strong rebound driven by improved risk appetite and renewed confidence in technology stocks.

Market Update and the Week Ahead

The upcoming week centers on critical US data—ISM PMIs, the ADP employment report, and PCE inflation—all of which could influence expectations for a December rate cut. European indicators such as CPI and industrial production will shape near-term movement in the euro and Swiss franc.

In Asia, markets focus on the Bank of Japan governor’s remarks and Australia’s investment and GDP data. AUD and NZD remain supported by resilient domestic fundamentals. Precious metals and US equities appear positioned to benefit further from strong structural demand and contained volatility as investors await clearer signals from central banks.

Market Drivers for the Week Ahead

Markets this week will be guided by a combination of central bank expectations and macroeconomic releases. The Federal Reserve remains positioned for a potential 25-bp cut, though incoming data could shift the outlook.

Across Europe, a stable inflation backdrop and neutral policy stance continue to support the euro and Swiss franc. The UK transitions from short-term budget reaction to anticipation of the BoE’s easing cycle, leaving the pound exposed to mild downward pressure.

In Asia, the BoJ’s slow normalization trajectory keeps the yen weak unless global volatility spikes. AUD and NZD are supported by improving growth impulses and remain favored against low-yielding currencies. Precious metals and US equities benefit from steady investment demand and low volatility conditions.

Currency Outlook

🇺🇸 US Dollar (USD)

The dollar faces a decisive week as ISM PMIs, ADP employment, and PCE inflation data could alter market expectations for a December rate cut. Supported equity markets and falling volatility create a mild downside bias unless data significantly outperforms.

US ADP and Interest Rate

🇪🇺 Euro (EUR)

The euro remains supported by stable economic conditions and a credible ECB policy hold. CPI and industrial figures from the euro area may introduce short-term volatility, but overall resilience is expected against currencies tied to more aggressive easing cycles.

🇬🇧 British Pound (GBP)

The pound remains sensitive to the BoE’s upcoming easing cycle alongside softer UK growth prospects. Any rallies are likely to encounter selling pressure unless new economic data provide upside surprises.

🇯🇵 Japanese Yen (JPY)

The yen continues to function as a funding currency, with limited upside unless a risk-off event forces position unwinding. BoJ policy remains near the lower bound, keeping sustained appreciation unlikely.

🇨🇦 Canadian Dollar (CAD)

The Canadian dollar benefits from improving GDP and employment data but remains vulnerable to global commodity trends. Any upside surprise in domestic employment or inflation could strengthen CAD further in the short term.

🇦🇺🇳🇿 Antipodeans (AUD & NZD)

AUD and NZD remain supported by resilient domestic data, strong investment signals, and balanced central bank policies. Both currencies hold relative value opportunities versus low-yielders or currencies in clear easing cycles.

Precious Metals (Gold & Silver)

Gold and silver remain well supported by strong institutional demand, expectations of gradual Fed easing, and modest volatility. Any short-term dips are likely to be viewed as opportunities to buy.

U.S. Equities

US equity indices benefit from recovering risk sentiment and the robust performance of AI-related sectors. The path of least resistance remains higher barring significant macroeconomic or geopolitical shocks.

Economic Calendar – Week Ahead

- 2025/12/01 – Monday

USD – ISM Manufacturing PMI

JPY – Japan Q3 Capital Expenditure - 2025/12/02 – Tuesday

EUR – Eurozone Flash CPI

GBP – UK Services PMI

AUD – Australia Manufacturing PMI (S&P Global)

USD – ISM Services PMI - 2025/12/03 – Wednesday

CAD – Canada Employment Data

CHF – Swiss Inflation

AUD – Australia Services PMI (S&P Global)

USD – ADP Employment Report - 2025/12/04 – Thursday

USD – Challenger Layoffs

JPY – Japan Household Spending

EUR – German Industrial Orders

EUR – French Industrial Production - 2025/12/05 – Friday

USD – PCE Inflation

USD – Personal Consumption

EUR – Eurozone Revised Q3 GDP

CAD – Canada Employment Data

AUD – Australia Q3 GDP

Final Notes

The week ahead will be heavily influenced by US economic releases and shifting expectations for central bank policy decisions. The dollar may remain under pressure if labor and inflation data soften, while the euro, pound, and Swiss franc receive support from their respective stable monetary settings. AUD and NZD continue to offer attractive positioning opportunities backed by strong domestic fundamentals.

Precious metals and US equities benefit from persistent structural demand, although sudden shocks remain a risk. Traders should maintain disciplined risk management, avoid over-leveraging, and closely track event-driven volatility throughout the week.