Global markets ended the previous week under heavy pressure as concerns over stretched AI valuations, increasingly hawkish Federal Reserve commentary, and a lack of clean economic data—caused by the prolonged U.S. government shutdown—pushed investors toward risk-off positioning. Major U.S. equity indices fell as much as 5.5% to 8.5% from recent peaks, while even a strong earnings report from Nvidia failed to spark sustainable optimism. Meanwhile, the U.S. Dollar benefited from defensive flows, the Japanese Yen approached intervention-risk levels, and both oil and gold fell after headlines suggesting a potential Ukraine–Russia ceasefire.

The week ahead brings a quieter U.S. calendar due to the Thanksgiving holiday, meaning thin liquidity could amplify market volatility. Key U.S. releases such as PCE inflation and consumer confidence may determine whether investors can rebuild risk appetite—or double down on caution. Alongside them, the UK Budget, Tokyo inflation, Canada’s Q3 GDP, and Australia’s CPI are among the major events likely to shape FX market sentiment.

Key Points

- Global equities sold off sharply amid AI valuation concerns and hawkish Fedspeak.

- The U.S. Dollar strengthened as risk sentiment deteriorated, but its direction now hinges on PCE and consumer confidence data.

- Thin liquidity during the U.S. Thanksgiving week could exaggerate market moves.

- Intervention risk for the Japanese Yen is rising as USD/JPY approaches critical levels.

- The UK Budget is the most important risk event for the British Pound this week.

- Canada’s Q3 GDP, Australia’s CPI, and the RBNZ meeting may reshape the outlook for commodity currencies.

- A potential Ukraine–Russia truce weighed heavily on oil and gold prices.

Week in Review

Markets ended the previous week on shaky ground as several risk factors converged. Investors grew increasingly uneasy about elevated valuations in the AI sector, with major U.S. equity benchmarks falling sharply—at one point between 5.5% and 8.5% below their recent highs. One-month implied volatility spiked to fresh monthly levels, signaling a market preparing for turbulence rather than stabilization. Nvidia’s strong earnings and upbeat commentary provided only temporary relief, as traders questioned whether AI leaders can realistically execute their massive capital-expenditure ambitions.

In U.S. macro news, the delayed September nonfarm payrolls report painted a mixed picture: job gains were stronger than expected at 119,000, but the unemployment rate climbed to 4.4%, a new cycle high. The lack of clearer October and November data—still delayed due to the shutdown—has deepened disagreements within the FOMC. Hawks pointed to resilient labor demand, while doves stressed downward revisions, concentration of job growth, and weakening household demand. As a result, expectations for a December rate cut swung sharply throughout the week.

Across Europe, the Euro struggled as ECB officials signaled comfort with their current policy stance. The British Pound weakened ahead of the upcoming Budget announcement, with concerns about the UK’s fiscal position and lingering signs of economic slowdown weighing heavily. The Japanese Yen faced renewed pressure as USD/JPY surged toward key intervention zones, with verbal warnings from Japanese officials intensifying.

Commodity markets reacted strongly to geopolitical developments. Reports of a potential U.S.-brokered Ukraine–Russia ceasefire pushed oil and gold lower, despite broader risk-off sentiment. Gold fell toward the 4,000 mark, showing difficulty benefiting from equity weakness. Bitcoin suffered even more dramatically, losing 18% on the week—its worst weekly performance since November 2022.

Market Update & The Week Ahead

The new trading week begins with global markets still digesting last week’s heavy risk-off tone. Concerns over inflated AI valuations, the fragmented flow of U.S. economic data, and sharply shifting expectations for rate cuts have kept investors defensive. With Thanksgiving creating a shortened U.S. trading week, market liquidity will thin significantly, increasing the likelihood of exaggerated price swings.

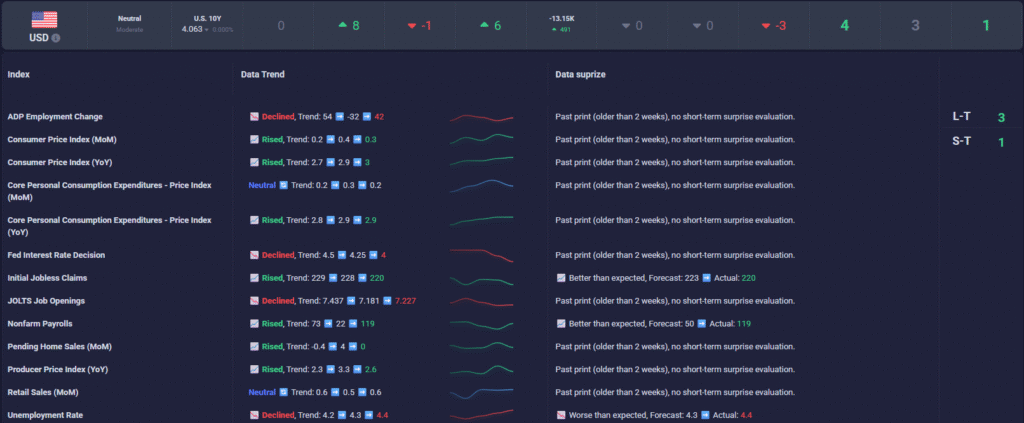

US Macroeconomic data 24 nov 2025

The central question for markets is straightforward yet critical:

Can incoming U.S. data help revive risk appetite—or will thin liquidity amplify another wave of risk aversion?

The spotlight will be on the upcoming PCE inflation report and consumer confidence figures. Both releases carry strong potential to determine whether December’s rate-cut expectations regain traction or fade entirely. Beyond the U.S., major macro catalysts include the highly anticipated UK Budget, Japan’s Tokyo CPI, Canada’s Q3 GDP, and Australia’s CPI inflation print.

This combination of low liquidity and high-impact events creates a landscape where both opportunities and risks will appear sharply. Active traders will likely face a week in which timing and disciplined risk management matter more than ever.

Key Drivers for the Coming Week

1. U.S. PCE Inflation & Consumer Demand Signals

The absence of October CPI—due to prolonged shutdown delays—has shifted full market attention toward the PCE report. With policymakers openly divided and positioning extremely sensitive to incoming data, PCE may determine whether December remains a viable meeting for easing. A softer PCE print could revive risk appetite and weaken the Dollar, while a firmer reading would reinforce the hawkish narrative and strengthen the Dollar.

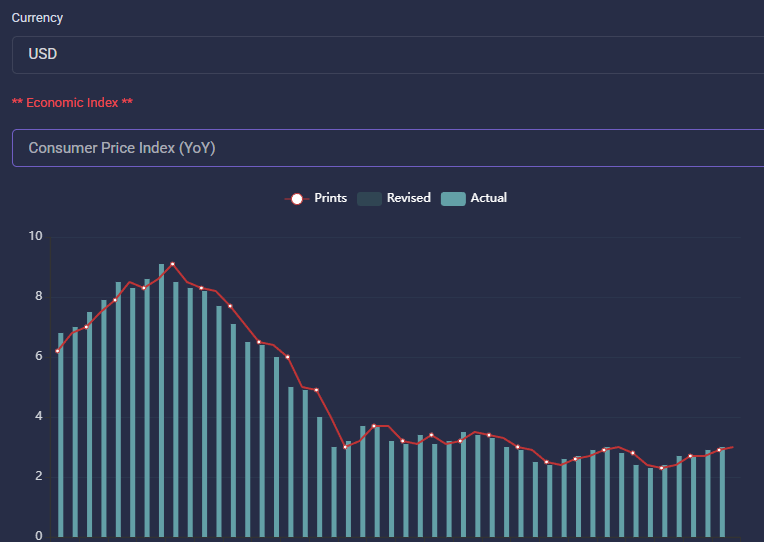

US CPI YoY

Consumer confidence could be an even more important determinant for Q4 GDP forecasts. Weaker household sentiment would reinforce concerns that the shutdown and tighter financial conditions are already weighing meaningfully on spending.

2. Geopolitics: Ukraine–Russia Ceasefire Prospects

The tentative, U.S.-brokered peace proposal has already pushed oil and gold sharply lower. A meaningful escalation—or a collapse in negotiations—would be a major volatility trigger.

Progress toward peace: Bearish for oil & gold, supportive for risk assets

Breakdown in negotiations: Bullish for oil & gold, negative for equities and risk currencies

Given thin liquidity later this week, even small geopolitical headlines may generate outsized market reactions.

3. UK Budget and Fiscal Policy Shock Risk

Wednesday’s UK Budget may be the most market-moving event for a single currency this week. Chancellor Rachel Reeves faces a £20bn fiscal gap, and any combination of tax hikes or spending cuts will deeply affect markets.

A tax-heavy budget may boost gilts short-term but risk political instability and weaken GBP.

A soft or “light-touch” budget may disappoint investors seeking fiscal discipline, also weakening GBP.

In short, the British Pound enters the week in a fragile state.

4. Japanese Intervention Risk

USD/JPY approaching the 158–160 zone heightens the threat of direct intervention. Verbal warnings have intensified, and with liquidity thinning later in the week, Japanese authorities may see a window for deeper impact. Tokyo CPI on Friday could add more pressure if it surprises on the upside.

5. Commodity Currency Catalysts: CAD, AUD, NZD

Canada: Q3 GDP carries added uncertainty due to missing trade data caused by the U.S. shutdown. Weak numbers would reinforce expectations that the Bank of Canada remains sidelined.

Australia: CPI may determine whether the RBA reconsiders its recent tone. AUD is best positioned among commodity FX to benefit from renewed Dollar weakness—if inflation holds firm.

New Zealand: The RBNZ remains on an easing trajectory. Unless the bank delivers a meaningful hawkish shift, NZD likely remains the weakest among its peers.

FX Outlook for Major Currencies

🇺🇸 US Dollar (USD)

The Dollar strengthened last week as risk appetite collapsed and uncertainty surrounding December’s rate-cut outlook intensified. The inconsistent September payrolls report offered little clarity, leaving Fed officials divided.

This week:

A soft PCE or weak consumer confidence → USD likely dips

A strong PCE or hawkish Beige Book → USD likely strengthens

The Dollar remains hypersensitive to risk sentiment and Fed repricing.

🇨🇦 Canadian Dollar (CAD)

Canada’s latest data show fading economic momentum: slowing housing starts, weak retail sales, and sticky underlying inflation. With uncertainty around delayed trade data, the upcoming Q3 GDP release may face significant revisions.

Outlook: CAD remains vulnerable unless GDP surprises to the upside or oil prices rebound—both currently unlikely.

🇬🇧 British Pound (GBP)

The Pound faces a pivotal week. GBP weakness has intensified as markets brace for fiscal tightening, potential political fallout, and a slowing economy. Rising gilt yields reflect investor anxiety.

Key risk: Wednesday’s Budget is a potential “make-or-break” moment.

Any combination of aggressive tax hikes, insufficient consolidation, or political instability could push GBP lower against both USD and EUR.

🇪🇺 Euro (EUR)

The Euro remains range-bound, supported by steady ECB communication but undermined by subdued economic momentum and Dollar strength. Attention turns to Germany’s preliminary inflation report—a key input for the ECB’s final meeting of the year.

Outlook: Without a major upside surprise in inflation, EUR is likely to remain defensive.

🇯🇵 Japanese Yen (JPY)

The Yen continues to weaken as BoJ officials deliver mixed signals and U.S.–Japan rate divergence persists. PM Takaichi’s newly announced stimulus package adds further downward pressure.

Critical factor:

If USD/JPY breaches 158.66, intervention probability rises sharply—especially in a thin market.

Tokyo CPI may provide temporary support only if inflation exceeds expectations.

🇦🇺 Australian Dollar (AUD)

AUD suffered last week but may have one of the clearest pathways to recovery if domestic inflation surprises higher. A firm CPI print could force the RBA to adopt a more hawkish stance, which the market might reward quickly.

Outlook: Potential recovery candidate—data dependent.

🇳🇿 New Zealand Dollar (NZD)

NZD remains the weakest commodity currency. The RBNZ is firmly on an easing path and unlikely to pivot meaningfully this week.

Unless the central bank shocks markets with a hawkish shift, NZD’s trajectory remains downward.

Economic Calendar – Week Ahead

Monday – 2025/11/24

USD – Chicago Fed National Activity Index

EUR – Eurozone Consumer Confidence (Final)

Tuesday – 2025/11/25

USD – Consumer Confidence Index

USD – S&P/Case-Shiller Home Price Index

NZD – RBNZ Rate Decision

CAD – BoC Member Speeches (if scheduled)

Wednesday – 2025/11/26

USD – Preliminary PCE Report

USD – Beige Book

GBP – UK Budget 2026 (Major event of the week)

EUR – Germany Initial Inflation Report

CAD – Q3 GDP Growth

Thursday – 2025/11/27 (U.S. Thanksgiving – Low Liquidity Day)

JPY – Tokyo CPI

AUD – Business Activity Indicators

CNY – China Industrial Profits

USD – U.S. markets closed

Friday – 2025/11/28

USD – Early close for Black Friday

EUR – Eurozone Economic Sentiment Indicators

JPY – Japan Industrial Production

Final Notes

The upcoming week presents an unusual blend of low liquidity and high-impact macro catalysts, a combination that often leads to outsized volatility. With U.S. markets partially closed for Thanksgiving, price swings may exaggerate even modest data surprises or geopolitical headlines. U.S. PCE data and consumer sentiment will play a decisive role in shaping expectations for the December FOMC meeting, while the UK Budget could be a defining moment for the British Pound.

In the Asia–Pacific region, the Japanese Yen faces elevated intervention risks, especially if USD/JPY climbs closer to the 158–160 zone. Meanwhile, commodity-linked currencies such as AUD, NZD, and CAD may experience directional moves tied to CPI readings, GDP releases, and central bank decisions.

Risk Disclaimer

As always, traders should approach the week with heightened caution. Market conditions can shift rapidly, and the information contained in this analysis is intended solely for educational and analytical purposes—not as trading advice. Every trader must manage their positions based on personal risk tolerance, strategy, and market conditions.